Insights

Private credit under stress: Idiosyncratic episodes or systemic risk?

How to interpret recent valuation, liquidity, and governance stresses in private credit

April 2026

Ramu Thiagarajan

Head of Thought Leadership

Recent episodes have forced investors to confront an uncomfortable but necessary question — are these idiosyncratic stresses within private markets, or do they point to more serious systemic issues across the asset class?

Over the past several months, the insolvency at a UK-based private lender,1 asset markdowns at publicly graded Business Development Companies (BDCs), a permanent shift in redemption structure at a major non-traded credit fund,2 and repricing in software-heavy leveraged loan portfolios have dominated financial news headlines globally. Individually, each can be explained away. Taken together, they raise a more rigorous question — are these isolated incidents, or signs of deeper structural damage beneath a US$2–3 trillion market?

The answer matters not only for credit investors, but also for global financial infrastructure firms whose revenues are now deeply embedded in private credit's operating architecture. This distinction is critical as it determines whether recent headlines should be interpreted as manageable credit noise, or as evidence that one of the fastest-growing segments of modern finance carries vulnerabilities the market has yet to fully price in.

The taxonomy of recent stress

A closer look at recent episodes reveals three distinct archetypes, each carrying different implications for the broader market. Importantly, these do not share a single underlying cause. That diversity matters, as it reduces the likelihood that recent stresses propagate directly into systemic risk. We examine each of these briefly.

Platform governance in bilateral lending

The first archetype involves a breakdown in operational controls and governance at the platform level within bilateral lending arrangements that operate within different governance and oversight frameworks than diversified, institutional-grade credit platforms. While such arrangements can be highly structured and contractually robust, idiosyncratic issues can arise in segments where risk management, collateral verification, and governance are concentrated at the platform level rather than embedded across a diversified institutional framework. In a recent blog post,3 State Street Investment Management frames this category well. The difficulties of an individual lender or platform should generally be viewed as idiosyncratic and operational in nature, rather than evidence of broad credit deterioration.

A recent UK case illustrates this clearly. In early 2026, a UK-based private lender, Market Financial Solutions Ltd., entered insolvency with administrators subsequently obtaining a worldwide freezing order against its founder following allegations of fraud involving collateral allegedly pledged simultaneously to multiple counterparties. The scope of this episode appears contained — the firm operated in a segment structurally distinct from the diversified private credit market.

This type of episode underscores the importance of platform-level due diligence and the structural differentiation within private credit. Platforms with independent collateral verification, diversified underwriting, and robust legal protections exhibit materially different risk profiles than single-platform bilateral lending models. For allocators, the practical takeaway is that the “private credit” label encompasses a wide range of operational and governance standards, and differentiation at the platform level is a critical part of the underwriting process.

Credit quality deterioration in sector-concentrated portfolios

The second archetype involves credit stress emerging in portfolios with concentrated sector exposures — particularly where cyclical headwinds intersect with secular disruption. This is the pattern visible today in BDC markdowns and software-heavy leveraged loan portfolios.

BDC markdowns reflect the interaction of two forces. The cumulative effect of higher interest rates has weighed on borrower debt-service capacity across fixed income markets, including private credit portfolios, and an emerging AI-driven disruption has challenged the resilience assumptions embedded in recurring-revenue software business models. Technology now comprises approximately 20 percent of BDC holdings and CLO collateral; however, this declines to 15 percent in broadly syndicated loans (BSL) CLOs. Adoption of AI is inherently disruptive to incumbent technologies, increasing the risk of selective markdowns in affected portfolios. A recent study suggests that default rates could be substantial in a tail AI-disruption scenario.4 This represents cyclical credit strain occurring within a sector undergoing secular disruption. That combination is largely sector-specific, making it difficult to infer systemic stress for private credit as a whole.

Vehicle design: Liquidity mechanism stress

The third archetype involves the interaction between investor liquidity expectations and the liquidity profile of underlying credit assets. This is a matter of vehicle design and investor understanding, rather than credit quality.

Non-traded, perpetual-life BDCs typically offer investors quarterly redemption windows, generally capped at around 5 percent of net asset value, with provisions for a pro-rata scaling if requests exceed the cap. These 5 percent limits are set by design. This is to help investors meet liquidity needs while preserving the value-accretion attributes of long-term capital. When the demand for liquidity significantly exceeds this threshold, the GP is faced with several choices, including temporary redemption suspensions, pro-rata distributions or forced liquidations, either of a portion of the portfolio, or to accelerate the end of life of the BDC.

These mechanisms function as designed. Gates and redemption queues should not automatically be interpreted as indicators of credit stress, but as structural features intended to align liquidity with underlying asset duration. This feature of BDC designs is typically well understood by institutional investors.

The challenge arises when redemption requests by individual investors exceed gating limits, generating dissatisfaction despite contractual disclosure and design intent. Managers then face a conundrum between investor satisfaction, with implications for future business, and selling the assets or finding other means to meet the redemption requests.

Broadly, these perpetual-life BDCs have grown rapidly — industry data5 shows a 73 percent year-over-year increase in AUM to $226 billion across 41 funds as of Q1 2025. Overall BDC market AUM reached US$475 billion, with non-traded vehicles accounting for 65 percent of the total. The investor base remains approximately 80 percent institutional, which is a stabilizing factor, though the landscape is shifting at the margin as high net worth individual investor-oriented products (perpetual-life BDCs) continue to scale. Given these investors may operate on shorter time horizons than traditional institutional, the continued growth of individual-investor-oriented vehicles reinforces the importance of investor education around commitment duration, liquidity constraints, and redemption dynamics.

While the three stresses have distinct root causes, they share one condition in that they exist in an ecosystem where opacity makes it systemically difficult to distinguish noise from signal — until the signal becomes unmistakable — a time when systemic risks are well entrenched.

The five systemic risks

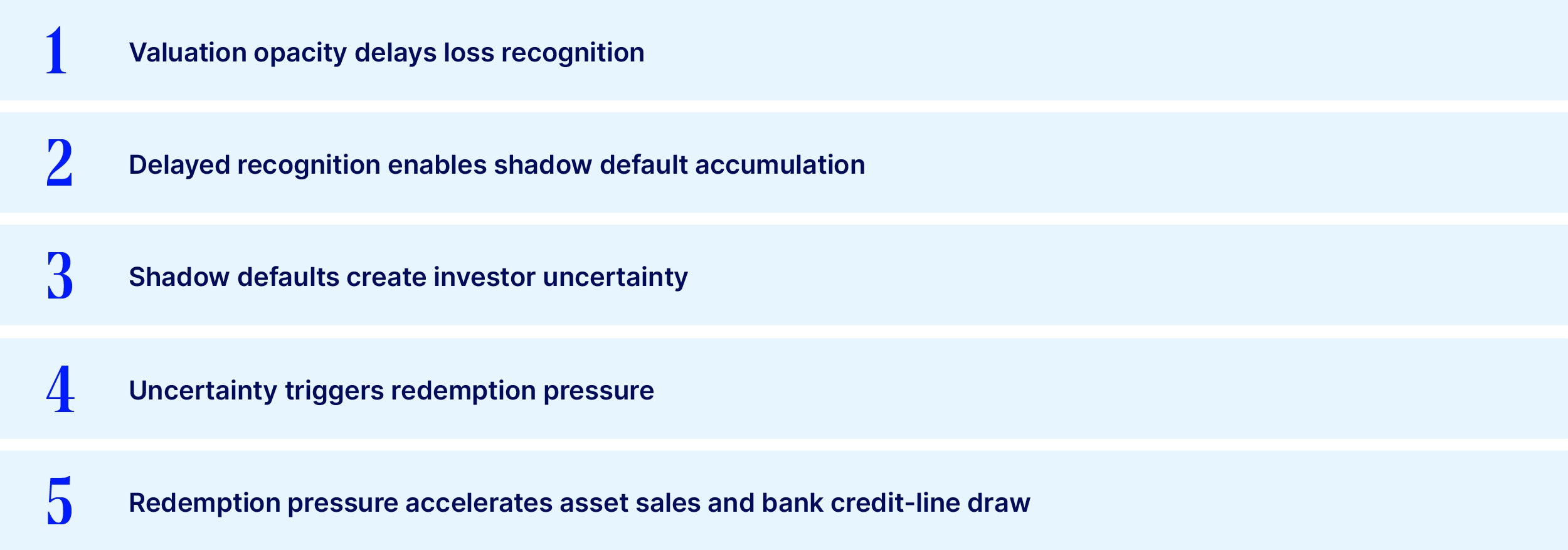

Beneath the individual episodes, five structural vulnerabilities are trending adversely and could form a connected amplification chain. The chain operates in this manner. Valuation opacity delays loss recognition. Delayed recognition enables shadow default accumulation. Shadow defaults create investor uncertainty. Uncertainty triggers redemption pressure. Redemption pressure accelerates asset sales and bank credit-line drawdowns. Those drawdowns transmit stress into the regulated banking core. As noted in the figure below, the chain is logical. Its activation requires only the right coincident shock. We examine some key aspects of this below.

1. Valuation opacity

As is well known, private credit is typically marked to model periodically and not to a continuously traded market. Thus, growing discounts to NAV emerge more slowly in reported NAVs even when asset class depreciation is occurring quickly underneath. Stale marks suppress measured volatility, obscure true correlations, and create incentives for investors to redeem before valuations catch up. In benign conditions, that opacity is tolerated. Under stress, it becomes the trigger for a sharp, discontinuous loss of confidence. This loss of confidence can result in a negative spiral of redemption requests. These differences in value between liquid securities in vehicles containing illiquid assets, including but not limited to private credit, are indicative of the relatively long term nature of those assets, and can cut both ways, with the value of the portfolio outstripping that of the vehicle over the periods in which they are valued.

2. Shadow default accumulation

Formal default rates are increasingly poor diagnostics for distress in private credit. More revealing signals include payment-in-kind structures, covenant amendments, and selective defaults that postpone recognition without resolving the underlying problem. The data is striking. The share of investments carrying payment-in-kind (PIK) interest (signaling deferred rather than genuine cash generation) rose from 2.5 percent in Q4 2021 to 6.4 percent by Q4 2025.6 While these are not default statistics per se, they are leading indicators of defaults not yet forced into recognition.

3. Retail liquidity mismatch

Private credit historically relied on institutional capital with long lockups. Illiquid credit paired with redemption-sensitive capital creates first-mover incentives that do not exist in committed structures. This dynamic does not replicate a bank run precisely — but it rhymes with one. The creation of these semi-liquid structures increases the need for investor education around longer term commitments for realizing value in these types of investments. Semi-liquid credit funds in the US have grown from US$75 billion in assets in 2022 to US$188 billion in 2024.7

4. CLO technical amplification

Technology and software exposures concentrated in CLO collateral create binary trigger risk arising from AI and hence stresses can be correlated. If correlated downgrades push large volumes of loans into CCC buckets, over-collateralization tests can fail, and cash flows can be diverted abruptly. Roughly 4 percent of private-credit CLOs were in breach of junior overcollateralization (OC) tests in Q3 2025,8 while the overwhelming majority remained compliant. That distinction may not hold under simultaneous sector stress. These triggers do not deteriorate gracefully.

5. Bank-NBFI interconnection

Bank loans to non-depository institutions such as asset managers and private credit firms grew from US$322 billion in 2015 to US$1.28 trillion by 2025,9 with over half of commitments reportedly undrawn.10 Those undrawn lines are the latent propagation channel: concurrent draws under stress hit regulated bank balance sheets directly, transforming a private credit event into a broader financial system concern. Notably, research11 finds that the network of interconnections in the financial system involving private credit is more distributed, which could amplify shocks during the time of market stress.

Key takeaways: Why context matters in private credit

The central question is whether these stresses are idiosyncratic or capable of propagating through the system and affecting private credit more broadly. That framing, however, is too binary.

The episodes are idiosyncratic in nature. The UK lender collapse was a matter of governance. BDC markdowns reflect sector-specific credit strain compounded by rate normalization. The redemption restructuring was a vehicle-design issue amplified by investor behavior. None of these, on their own, indicate a generalized credit event.

But the conditions in which they occurred — valuation opacity, growing individual investor participation in illiquid structures, compressed spreads, and concentrated sector exposures — are structural features of the current market that could amplify future shocks if they arrive. The probability of systemic episodes appears low given the strength of underlying corporate profits, contained default rates, and a meaningful absorption buffer in the form of industry dry powder. State Street Investment Management characterizes the current environment as one of “adjustment and repricing rather than broad-based dislocation.”

The more useful question for the next twelve to eighteen months is not whether isolated incidents will continue — they will. It is whether the macroeconomic environment allows them to remain contained, or whether coincident shocks reveal structural damage that private credit's opacity has, until now, successfully obscured.

In markets without a closing bell and real-time valuation, the discipline of monitoring is everything. The investors and allocators who build rigorous frameworks for tracking the right leading indicators — PIK trends, NAV markdown frequency, redemption dynamics, OC test margins, and bank exposure data — will be measurably better positioned when the next episode arrives. And the managers who prioritize transparency, diversified portfolio construction, and alignment of investor liquidity with underlying asset duration will be the ones who emerge from this period with their credibility enhanced.

Acknowledgements

The author would like to thank Donna Milrod, James Jefski, Jennifer Bender, and Hanbin Im for detailed comments on earlier versions of the paper. Priyaam Roy, Hanbin Im and Prashant Parab provided excellent research assistance. Thanks also to James Redgrave, Anna Bernasek, and Eric Garulay for their help in carefully reviewing earlier versions of this paper and providing insightful comments.