April 2026

2026 Global ETF Outlook:

From wrapper to backbone

The ETF marketplace entered 2026 with a rate of acceleration that is changing the conversation, from whether ETFs will keep expanding to how the ecosystem will support what comes next. Learn about the global and regional trends in ETFs that will matter most this year from State Street’s ETF team.

In 2025, the global ETF marketplace climbed to almost US$20 trillion, with record inflows and a record number of new ETFs listed globally — clear signals that ETFs are scaling not just in size, but in reach and relevance. That momentum — and our vantage point on it — sets the foundation for this 2026 report. Informed by State Street’s internal research, ongoing client and stakeholder discussions, and participation in industry committees and innovations, this report synthesizes the major forces shaping ETF markets in 2026 and outlines strategic imperatives for issuers, investors, and ecosystem partners.

This year, the most important ETF story won’t be simply “more” — it will be “more” and “fundamentally different.” ETFs are expanding the investable universe, bringing increasingly sophisticated strategies and asset classes into a liquid, transparent wrapper. As that universe broadens, however, so do the practical questions that determine who wins: how to manage product complexity, how to manage capacity and liquidity constraints, and how to translate innovation into repeatable distribution.

This outlook is designed to be practical — an input you can use across planning conversations, product roadmaps, and stakeholder engagements. You’ll find:

- A global outlook that frames what’s changing

- Regional megatrends to highlight how growth drivers diverge across major geographies

- Our market predictions for 2026

- A curated set of external partner perspectives across the ecosystem

With so much in motion, our focus is on helping you move from insights to execution. The State Street ETF team is ready to engage — globally and locally — to support the strategic and operational decisions that will shape ETF growth, scale, and resilience in 2026.

Anna Bernasek

Head of Insights

Global outlook for ETFs

Frank Koudelka

Global Head of ETF Solutions

Jeff Sardinha

Head of ETF Solutions, North America

Ken Shaw

Head of ETF Solutions, EMEA

Ahmed Ibrahim

Head of ETF Solutions, APAC

We titled State Street’s 2025 Global ETF Outlook “The expansion accelerates.” As the year unfolded, the framing proved to be spot on. Multiple records were set in 2025, powered by shifting investor preferences, structural and product innovations, and the expansion of ETF use cases across both institutional and retail channels (see Box 1). The ETF story is resonating, and many global asset managers have moved from viewing ETFs as a “side experiment” to embracing them as a core component of their distribution strategy.

ETF managers are broadening access to asset classes and increasingly complex strategies previously limited to private wealth, institutional channels, or hedge funds. This expansion is well timed as advisors are leaning more heavily on ETFs as core building blocks, capable of anchoring nearly every component of modern advisory solutions. The market has responded with a wave of new entrants and product launches, including several industry firsts. And while regulatory tailwinds continue to support innovation, expectations are rising around stronger oversight, clearer frameworks, and enhanced investor protections.

What does all this growth, innovation, and increasing complexity mean for 2026? We see three key trends shaping the ETF marketplace globally:

- A growing tension between access and structure: As ETFs broaden investor access to new strategies and asset classes within a liquid wrapper, complexity — and the need to manage capacity constraints — are becoming increasingly critical.

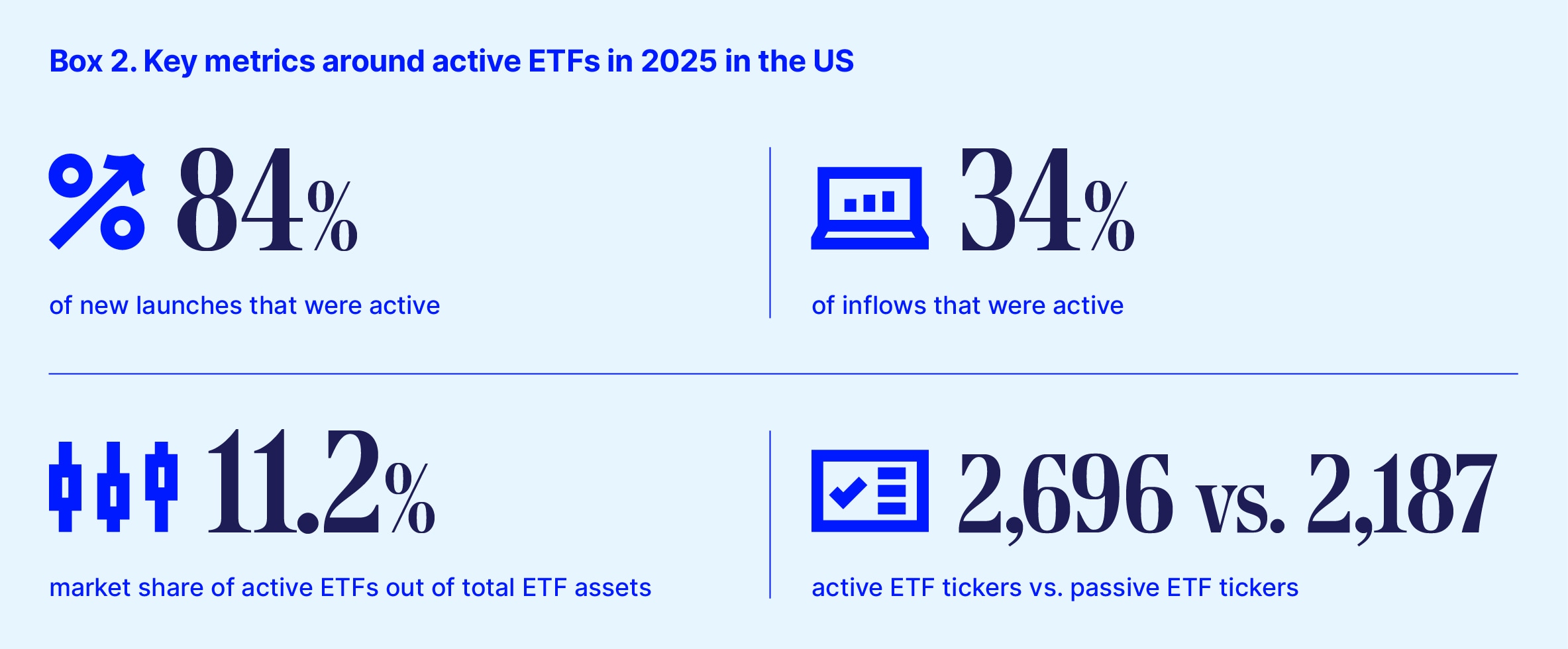

- Accelerating active adoption: Active ETFs, particularly active fixed income and outcomes- and derivatives-based strategies, remain the global product center of gravity.

- The rising importance of infrastructure and distribution: Share classes, conversions (351s), and distribution economics are the infrastructure story that will determine the pace of adoption.

In 2026, the ETF growth and innovation story continues — with a twist. While new constraints are emerging, ETFs are still advancing across markets and geographies. No longer just a wrapper, ETFs are becoming the backbone of portfolios and market structure.

Megatrends by region

Across North America, Europe, and Asia Pacific, the 2026 outlook for ETFs converges on a common theme: ETFs are evolving from core beta tools into the default distribution and implementation layer for modern investing. While the direction is consistent, the “why” and “where” momentum concentrates differ by region.

North America is defined by scale and innovation. After back-to-back years of US$1 trillion2 inflows in the United States and record Canadian inflows, issuers are pushing the wrapper into ever more complex territory.

In Europe, the outlook is one of market maturation and broadening adoption. A record 2025 sets the stage for 2026, with active ETFs emerging as the defining product momentum story3 — still representing only approximately 3 percent of assets, but accounting for a rapidly growing share of flows and new launches. The investor narrative is increasingly retail-led, as ETFs become more deeply embedded in long-term savings and retirement structures. This momentum is reinforced by supportive policy direction and new access routes, including white-label solutions and renewed focus on share-class structures.

APAC also shares the growth narrative, but it’s more market-diverse and regulation-shaped. The region’s ETF base is expanding from a larger passive foundation, with active adoption accelerating unevenly across markets. Australia is scaling rapidly as global managers import active lineups; China’s growth is driven by low-cost and thematic demand, supported by policy tailwinds; Japan’s adoption is structurally underpinned by tax-advantaged programs; and markets such as South Korea and Taiwan combine high retail participation with education and risk-management guardrails as active, leveraged, and thematic strategies proliferate.

Our market predictions

We now move beyond broad megatrends to make clear, trackable calls on how ETF markets are likely to evolve in 2026. These predictions reflect where momentum is building, where inflection points are emerging, and where change may arrive sooner — or later — than consensus expects. We will revisit these calls through the year to assess how market dynamics, regulation, and investor behavior are reshaping the global ETF landscape in real time.

North America in 2026

- US$2.1 trillion of inflows in US ETFs

- More US ETFs than mutual funds (ex MMF, and MF FOF)

- The top 10 issuers in the US on January 1 will not be in the same order by December 31

- We will see multiple acquisitions in the ETF space

- We will see the first US$1 trillion ETF

- US$750 billion inflows into active ETFs in the US, a 50 percent increase

- 85 percent of launches will be active

- Active fixed income will eclipse passive fixed income inflows

- Global and emerging market equity inflows will double in the US from 2025

- At least 12 firms will add ETF share class of a mutual fund or mutual fund share class of an ETF

- 100 mutual funds to ETF conversions will occur

- Canada will nearly double its ETF inflows from US$109 billion in 2025 to US$200 billion+ in 2026

- Active ETFs in Canada will eclipse US$200 billion in the first half of the year

Europe in 2026

- The European Exchange Traded Investment Product (ETP) market will grow by over 25 percent and reach US$4 trillion in AUM by the end of 2026

- 12-month European ETP net inflows to surpass US$500 billion

- Retail adoption will accelerate yet again, with average ownership rates increasing by at least 5 percent to 30 percent (from 25 percent average as of November 2025)

- Active ETF launches in region will outpace all passive product launches in 2026

- Active fixed income launches and flows will both exceed 40 percent of all active metrics in 2026

- A minimum of 15 new entrants, some with presence in other jurisdictions, others new to ETFs, with the majority coming to market doing so through active strategies

- Further potential consolidation in Europe with traditional managers and existing ETF issuers looking to acquire existing ETF issuers

- ETF issuer-led white label solutions to facilitate new issuers entering the market, will continue to expand, with at least one new issuer entering the space in 2026

- Continued utilization of the listed and unlisted share class model by both ETF issuers and mutual funds managers adding ETF classes — at least four managers will do so in 2026

- At least two new entrants will launch product in the Digital Asset ETP space. However, growth will continue to lag other jurisdictions (Crypto will remain an ineligible asset within the guise of the Eligible Assets Directive, though more regulators will follow the CSSF and allow Undertakings for Collective Investment in Transferable Securities [UCITS], within the limits of the 10 percent trash bucket, access crypto via crypto ETPs)

- An issuer will receive approval to launch a tokenized ETF

APAC in 2026

Australia

- Net inflows to surpass AU$40 billion, bringing total AUM close to AU$380 billion

- Both domestic and international fixed income strategies to increase market share

- Number of Australians that will hold ETFs in their portfolio to exceed three million

- At least two large global investment managers to enter the ETF market

- Established investment managers to increase adoption of dual access/ETF share class models to their existing suite of product offerings

China

- China to remain the biggest ETF market in region

- Growth to continue; however, it will be at a slower pace than 2025

- Updates to regulation will lower barriers to entry for foreign investors

- Active ETF strategies to see positive inflows through 2026

Japan

- Foreign inflows into Japan equities to remain positive throughout 2026

- Active ETF strategies to become more attractive to retail investors

South Korea

- Active ETF demand to remain the highest in APAC

- Total ETF AUM to exceed US$270 billion

Taiwan

- Total ETF AUM to exceed US$260 billion

- At least two large global investment managers to launch active ETF strategies

- Cryptocurrency ETF to debut in 2026

Hong Kong

- AUM to surpass US$100 billion

- Investor demand for active ETFs will likely see products on the Hong Kong Exchanges and Clearing Limited (HKEX) exceed 50 offerings

- Increase in investments in crypto/digital products will be evident through 2026

Industry predictions

Over the years, continuous innovation in the ETF industry has fostered deeper collaboration across the ecosystem, as stakeholders work closely together to deliver value for shared clients. We reached out to many of our industry partners to get their outlook for ETFs in 2026. Here is a selection of what they said curated according to key themes:

Related solutions

ETF Servicing

As ETFs scale and strategies grow more complex, execution matters. Our ETF Servicing Solutions support issuers across the full ETF lifecycle — from launch to growth — helping you scale with confidence.