Insights

June 2026

Structural rise in real interest rates: Treasury premium erosion and asset allocation implications

A structural rise in real interest rates is reshaping asset pricing, weakening diversification, and challenging the traditional defensive role of US Treasuries.

Ramu Thiagarajan

Head of Thought Leadership

Hanbin Im

Global Macro Researcher

Prashant Parab

Global Macro Researcher

Amar Jyoti

Global Macro Researcher

The post pandemic rise in real interest rates has unsettled a long standing macro regime defined by secular disinflation, global savings glut, and strong demand for safe and liquid assets. What initially appeared to be a cyclical normalization, has persisted even as inflation receded, raising the possibility that equilibrium real rates have shifted structurally higher. Recent discussions by monetary researchers1 and central bankers2 have increasingly pointed to the possibility of higher equilibrium real interest rates.

Real rates are at two-decade highs and are expected to rise further as inflationary impulses firm up globally, reflecting tariffs and energy market dislocations associated with recent geopolitical conflicts in Ukraine and Iran. This shift has significant implications for asset pricing, portfolio diversification, and the ongoing role of US Treasuries as the anchor of defensive allocations.

By decomposing real interest rates into their structural components and analyzing how asset sensitivities have evolved across monetary regimes, our analysis shows that the recent rise in real rates reflects a fundamental erosion of the extraordinary privilege of US Treasuries, reinforced by rising term premia, rather than temporary policy tightness alone. As a result, rising real interest rates have reemerged as a dominant cross asset pricing factor with important implications for strategic asset allocation.

Key findings include

- Structural rise in real rates: One of the key determinants of low real rates has been the convenience yield on US Treasuries, reflecting the extraordinary privilege enjoyed by the US Sovereign market. Since 2020, the increase in trend real interest rates has been driven primarily by a persistent decline in this convenience yield — across both safety and liquidity dimensions — alongside the re emergence of positive term premia.

- Fiscal dynamics matter: Persistent fiscal deficits, rising Treasury supply, and deteriorating debt dynamics have eroded the scarcity premium embedded in Treasuries, weakening a key force that suppressed real rates for decades.

- Weakened diversification: Real interest rates have become a dominant cross asset pricing factor in the post QE period, with equities, credit, commodities, and private assets exhibiting increasingly synchronized negative sensitivities.

- Equity regime shift: Equities, largely insulated from real rate shocks during the QE era, now display statistically significant negative exposure to rising real yields, materially reducing the effectiveness of traditional 60/40 style diversification.

- Selective resilience: The US dollar remains positively linked to higher real rates while energy linked assets and equity value strategies exhibit relatively more resilient return profiles.

Investment implications

- Rebuild defensive allocations: Diversification should rely less on long duration Treasuries alone and more on a broader defensive toolkit that includes safe haven currencies, commodities, and shorter duration assets.

- Adopt a regime aware framework: Asset correlations are increasingly sensitive to macro financial regimes; static allocation frameworks should give way to dynamic approaches informed by real rate and fiscal signals.

- Selectively optimize Treasury Allocation: Despite reduced hedging power, Treasuries remain critical for liquidity and collateral purposes but no longer serve as a reliable standalone hedge against risk off episodes.

Overall, the evidence points to a regime shift in which structurally higher real interest rates reshape cross asset return dynamics. Portfolio construction frameworks built for the low rate era may no longer deliver the intended diversification benefits, requiring institutional investors to recalibrate defensive strategies and reassess the central role of duration heavy assets in risk management.

Introduction

Quo vadis, r*? This question — posed by the Bank for International Settlements (BIS) in its March 2024 Quarterly Review3 — captures the defining uncertainty of the post-pandemic macroeconomic landscape. For two decades before the pandemic, the direction seemed clear: down. According to the Holston-Laubach-Williams (HLW) model, r* declined steadily from roughly 3.5 percent in the early 1990s to below 1 percent by the mid-2010s.4

The recent increase in estimates of the natural rate of interest — the unobservable real rate consistent with equilibrium between savings and investment, output at potential, and stable inflation — has become a central topic of debate among investors, central banks, and fiscal authorities. The discussion on r* is not just academic. This discussion is motivated by a sustained increase across most estimates of r* and meaningful reversal in real rates in the global economy.

The US 10‑year TIPS yield, at around 1.9 percent, is the highest in nearly two decades — alongside expectations that the federal funds rate will remain above 3.5 – 3.75 percent through 2026 and r* estimates that continue to trend higher. European Central Bank (ECB)’s Isabel Schnabel frames the debate as a contest between two hypotheses in her 2024 speech5: The savings-investment view, where demographics and productivity still anchor r* at lower levels, and the monetary policy view, where prolonged accommodation itself suppressed r* and its withdrawal has revealed a higher equilibrium.

This question is critical for asset allocation. If real interest rates have structurally risen, the negative equity-bond correlation that underpinned the 60/40 portfolio may have permanently shifted. If the rise is cyclical, current real yields offer the most attractive entry point for duration-seeking investors in nearly twenty years.

In this paper, we address the question from two empirical angles. First, we extend the decomposition of the real interest rate by Del Negro et al. (2017) through 2025 to identify which drivers have shifted and driven the increase in real interest rates. By decomposing the real interest rate into its underlying trend components, we assess whether the current increase reflects structural forces or cyclical dynamics. Second, we estimate period-specific relationships between asset returns and macro factors — real interest rate, inflation, inflation expectation, and growth — across three distinct periods — pre-quantitative easing (QE), QE, and post-QE periods, testing whether such relationship has shifted across different periods. Finally, we map the results of this analysis into actionable implications, equipping asset managers and asset owners with an empirical framework for strategic asset allocation in a world of competing equilibrium outcomes.

Decomposing the real interest rate: From trend to drivers

Across market‑based measures, model‑derived estimates, and survey‑based expectations, real interest rates in the United States have moved decisively higher since 2020. The 10-year TIPS yield has risen from approximately -1.1 percent at its mid-2021 trough to roughly 1.9 percent in April 2026. The HLW estimate of r* has edged higher, and survey-based measures compiled by the Federal Reserve Bank of Cleveland point in the same direction.6 While the rise in real interest rates is well established, the more important question is why they have increased, since the answer determines whether the shift represents a structural re‑anchoring or a cyclical deviation.

To answer this question, we turn to trend-cycle decomposition. A rise in the trend component of the real rate would signal a structural shift in the equilibrium — one rooted in persistent changes to the savings-investment balance, demographics, or the institutional demand for safe assets. On the other hand, a rise driven primarily by the cyclical component that may reflect tight monetary policy, a post-pandemic inflation shock, or transitory fiscal stimulus, would suggest that reversion to lower rates is likely once these forces abate.

To assess the structural vs cyclical trend we adopt and extend the analysis proposed by Del Negro et al. (2017) to decompose real interest rates into multiple components, including stochastic discount factor, convenience yield, and term premium. These are extracted from the joint dynamics of the nominal yields, real yields, inflation, and long-term expectations using a Vector Autoregression (VAR) model with common trends.7 This multivariate framework allows us to identify the drivers of shifts in the real-rate trend, rather than relying on univariate decompositions. The next section outlines this approach.

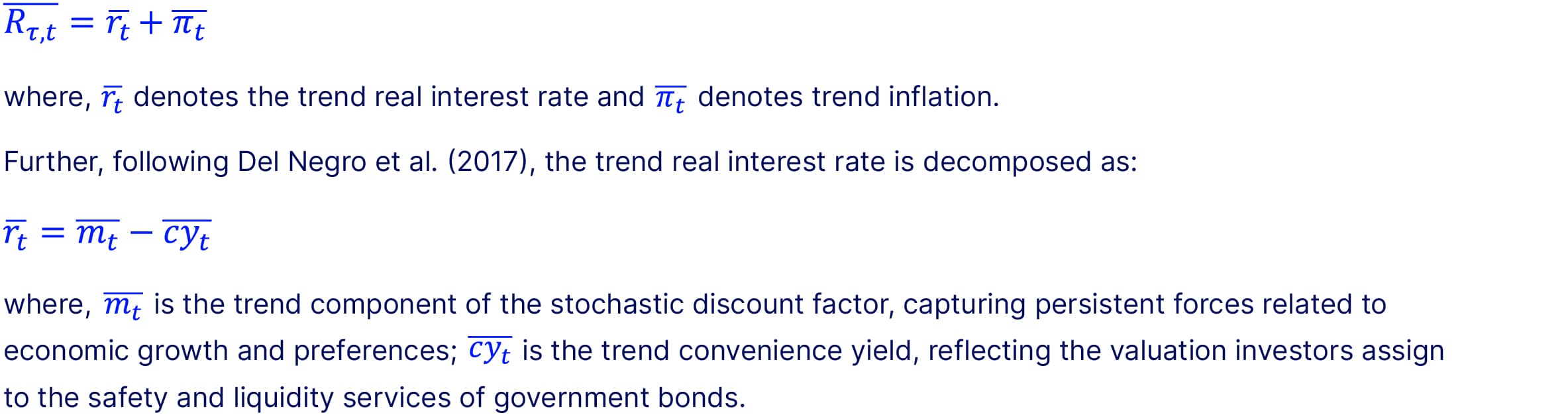

The nominal yield on a Treasury security of maturity τ can be decomposed into trend real rates and trend inflation:

The convenience yield is further decomposed into safety and liquidity components:

This decomposition allows long-run movements in real interest rates to be attributed either to changes in fundamental growth forces or to shifts in the demand for safe and liquid assets, which is central to assessing whether recent increases in real interest rates are structural or cyclical.

Extension of the Del Negro et al. framework to post-COVID period

Del Negro et al. (2017) (DN hereafter) decompose the secular decline in Treasury yields into three components: (1) a decline in trend real economic growth (stochastic discount factor), (2) an increase in the convenience yield —– the premium investors pay for the safety and liquidity attributes of Treasury securities, and (3) a residual capturing other forces. Their central finding was that increases in the convenience yield accounted for the largest share of the decline in the trend real interest rate, explaining up to one percentage point of the total 1.4 percentage point decline observed between the late 1990s and 2016.

Our extension of the DN framework to Q4 2025 shows that the picture has now reversed (Exhibit 1). The trend component of the real interest rate has been rising recently, and the primary driver of this increase appears to be a decline in the convenience yield across both safety and liquidity components (Exhibit 2). Notably, the liquidity component began to decline in 2018 and fell by approximately 20 percent from its peak by Q4 2025. In contrast, the safety component did not start to decline until 2022, registering an 11 percent decrease from its peak by Q4 2025. This finding is corroborated in the study by Szoke et al. (2024), which generalizes the HLW model by introducing the convenience yield as an explicit wedge between private borrowing costs and the safe rate and finds that the increase (and recent decline) in the convenience yield over the past two decades accounts for a large share of the decline (and recent increase) in r*. Recent decline in convenience yield of US Treasuries is also well-documented in the St. Louis Fed’s recent analysis8 and He and Krishnamurthy (2020). Put differently, a dominant factor behind the multi‑decade decline in real interest rates is now contributing to their reversal.

Why the convenience yield is falling: The fiscal channel and case for structural shift

The natural and important question is what is causing the convenience yield to decline. Our earlier work (Thiagarajan et al., 2025) on this topic finds that worsening US fiscal deficits and rising debt-to-GDP ratios are statistically significant drivers of the decline in the convenience yield, which was modeled following Du et al. (2018).

Krishnamurthy and Vissing-Jorgensen (2012) provide a rational explanation for this mechanism: the aggregate demand curve for Treasury securities is downward-sloping, so an increase in the supply of Treasuries — driven by persistent fiscal expansion — reduces the scarcity premium that investors assign to these securities. Li et al. (2025) establish a macro-financial model with endogenous fiscal policy, where the government finances deficit shocks partially through higher inflation expectations and partially through increased future borrowing, both of which reduce the convenience yield today. The feedback loop between the convenience yield and anticipated future debt supply amplifies the effect of fiscal shocks, creating a non-linear dynamic in which the convenience yield can decline more rapidly than the deficit expands.

A natural critique is that fiscal expansion may be driving real interest rates directly — through rising term premia or sovereign risk compensation — with the decline in the convenience yield a coincident byproduct rather than the operative transmission channel. We take this concern seriously but note that it does not contradict our framework. Consistent with Li et al. (2025), we treat the convenience yield not as exogenous but as the principal mechanism through which persistent fiscal expansion is priced into equilibrium real rates: deficits and rising Treasury supply lift real rates because they erode the scarcity premium investors assign to safe and liquid government debt. Supporting this interpretation, measures that isolate the safety and liquidity components independently of fiscal stance – the AAA–Treasury spread, the 10-year swap spread, and the Treasury premium derived from covered interest parity deviations (Du et al., 2018) – have compressed in the same direction and horizon as the trend decomposition.

Today’s fiscal arithmetic points more towards the structural interpretation in Li et al (2025). The Congressional Budget Office (CBO)’s latest projections9 estimate the federal budget deficit at $1.9 trillion in fiscal year 2026, which rises to $3.1 trillion by 2036. Federal debt held by the public is forecast to climb from 100 percent of GDP today to a record 108 percent by 2030 and 120 percent by 2036, surpassing the post-World War II peak of 106 percent set in 1946. Net interest payments on the national debt are projected to more than double from $1 trillion in 2026 to $2.1 trillion in 2036, rising from 3.3 percent to 4.6 percent of GDP. These are not cyclical projections that are expected to reverse with the business cycle but are likely to become structural shifts driven partly by the accumulated debt service burden of the past two decades of deficit spending. If the convenience yield is indeed a function of the supply of government debt, then the fiscal trajectory implies a sustained structural decline in the convenience yield and, by extension, a sustained structural increase in the real interest rate.10

Structural drivers of real interest rates: A literature survey

The literature emphasizes that real interest rates are shaped by a set of long-horizon structural determinants that operate largely outside the scope of our empirical analysis. In particular, Bernanke (2005) and Summers (2014) argue that sustained excess global saving relative to investment — driven by demographics, precautionary savings, and surplus accumulation in emerging economies — exerted persistent downward pressure on real rates. Holston, Laubach, and Williams (2017) show that these forces translated into a multi-decade decline in estimated neutral real rates across advanced economies, while Gamber (2020) and Carvalho et al. (2025) highlight the role of slower trend productivity growth and aging populations in lowering equilibrium real yields. In the post‑pandemic period, however, the drawdown of excess household savings coincided with a surge in public‑ and private‑sector investment, shifting the saving–investment balance and placing upward pressure on real interest rates.

Within this structural setting, it is important to assess the market pricing channels that translate these determinants into observed real yields that evolve dynamically across regimes. Krishnamurthy and Vissing Jorgensen (2012) show that US Treasuries provide safety and liquidity services that are priced as a convenience yield, lowering required real returns independently of macro fundamentals. During the QE period, this channel was reinforced by policy choices and market structure: Gagnon et al. (2011), D’Amico and King (2013), and Adrian, Crump, and Moench (2013) document how large scale asset purchases compressed term premia and reduced the amount of duration risk absorbed by the private sector.

The post-QE rise in real rates can be understood as a reconfiguration of these mechanisms rather than a departure from them. As demographics mature, global saving surpluses moderate (Del Negro et al., 2017), inflation volatility rises, and policy shifts from QE toward balance sheet normalization, the forces sustaining a large convenience yield weaken. Our results, outlined in the next section, speak directly to this margin in the literature: we show that the convenience yield component is empirically central and responsive to fundamentals, and that worsening fiscal dynamics and rising Treasury supply erode the scarcity value embedded in treasuries – mechanically lifting required real returns in the post-QE environment.

Real interest rates and asset returns across regimes

The preceding sections establish that the recent rise in real interest rates reflects more than a cyclical normalization from the post pandemic shock. Instead, the decomposition of real yields points to a structural erosion of the convenience yield, driven by worsening fiscal dynamics and rising Treasury supply, which mechanically raises the real rate required by investors. If real interest rates are indeed transitioning to a higher structural regime, the implications extend well beyond fixed income valuation and directly into the domain of strategic asset allocation.

Real interest rates enter asset pricing through multiple channels: discounting of future cash flows, relative valuation across risk assets, exchange rate adjustment, and portfolio substitution between safe and risky assets. A sustained upward shift in real rates therefore has the potential to reshape cross asset return patterns, alter diversification properties, and change the set of assets that hedge macroeconomic risk. Understanding these effects requires both a regime based perspective to characterize how average returns differ across real rate environments and a dynamic perspective, to quantify how changes in real rates transmit to asset returns within each regime.

We begin by examining average asset returns across three distinct real interest rate regimes — pre QE (Q1 2001 – Q4 2009), QE (Q1 2010 – Q4 2021), and post QE (Q1 2022 – Q4 2025) — which closely align with the evolution of the convenience yield documented earlier. We then turn to a regression based analysis to identify how the sensitivity of asset returns to real interest rate movements has evolved across these regimes, before assessing the implications for diversification through sectors and factors.

Average asset returns across real interest rate regimes

Average asset returns across real interest rate regimes highlight a clear structural transition in the investment environment (Exhibit 3). The pre QE, QE, and post QE periods correspond not only to distinct monetary policy frameworks, but to materially different configurations of real rates, inflation, and risk compensation, which are reflected in both the level and dispersion of returns across asset classes.

In the pre QE period (Q1 2000 – Q4 2009), asset performance was defensive and uneven. US equities generated slightly negative average returns, while Treasuries and credit delivered strong positive performance, consistent with declining real yields and repeated flight to safety episodes. Gold stood out as the dominant performer, reflecting heightened macro uncertainty and demand for real stores of value. Inflation sensitive assets and growth oriented equity segments generally underperformed, in line with weak growth and disinflationary pressures.

The QE period (Q1 2010 – Q4 2021) marks a regime of persistently negative real interest rates and elevated convenience yields. This environment was exceptionally supportive for risk assets. US equities, private equity, and credit all delivered strong double digit or high single digit average returns, while sector performance was broadly positive and dispersion compressed. Duration and growth sensitive assets benefited disproportionately from suppressed discount rates and abundant liquidity. In contrast, commodities underperformed, reflecting muted inflation dynamics and ample global supply. The defining feature of this regime was the breadth and uniformity of positive returns across asset classes.

The post QE period (Q1 2022 – Q4 2025) represents a sharp departure from this pattern. As real interest rates rose and remained elevated, average returns weakened across most duration sensitive assets. Treasuries delivered negative returns, investment grade credit returns compressed sharply, and high yield performance declined relative to prior regimes. Equity returns remained positive on average but fell well short of QE era outcomes, with noticeably higher cross sector dispersion. Private equity and private credit returns moderated materially, consistent with higher discount rates and tighter financial conditions.

By contrast, assets linked to real scarcity and inflation protection performed relatively well. Gold delivered its strongest average returns of any regime, commodities rebounded from QE era weakness. The US dollar posted modest positive returns, consistent with sustained real rate differentials.

Three themes emerge from the regime averages. First, the transition from QE to post QE coincides with a broad compression in average returns across duration sensitive assets, consistent with higher real rates acting as a structural headwind. Second, return dispersion increases materially in the post QE regime, signaling the breakdown of the policy driven compression that characterized the QE era. Third, real assets regained prominence, foreshadowing the central role of real interest rates in shaping asset performance going forward.

These descriptive patterns motivate the analysis that follows. The next section examines whether real interest rates have become an active pricing factor — rather than a coincident macro variable — by quantifying the sensitivity of asset returns to real rate movements across regimes.

Empirical framework: Isolating real-rate transmission to asset returns

To quantify the impact of real interest rates on asset returns, we estimate a set of period specific macro return regressions using both monthly and quarterly data from January 2001 through December 2025. The empirical framework is designed to isolate the effect of real interest rate movements while controlling for changes in risk, inflation, inflation expectations, and growth conditions. The regression equation for the analysis is given below:

Eq (1)11 where rt is the return on a particular asset at time t; ∆RIRt is the change in real interest rate from time t-1 to t measured by 10-year TIPS yield; ∆VIXt is the change in CBOE S&P 500 Volatility index from time t-1 to t; ∆Inft is the change in realized inflation measured by the US CPI inflation from time t-1 to t; ∆InfExpt is the change in inflation expectation from time t-1 to t measured as the difference between 10-year nominal US treasury yields and 10-year TIPS yields; and ∆Growtht is the change in growth proxy from time t-1 to t measured by the MSCI Cyclicals minus Defensive spread.

The key variable of interest — 10 year US TIPS yield — is used as an observable, market based proxy for long term real interest rates. Unlike model implied measures, TIPS provide a market-based measure of real yields that reflect both real rate expectations and risk premia.12

The analysis spans a broad cross section of assets, including US equities, government bonds, investment grade and high yield credit, commodities, currencies, and global equities. In addition, quarterly regressions incorporate private equity and private credit.13 To assess the economic importance of real rates relative to other macro drivers, we complement standard inference with a Shapley value decomposition of regression R², which measures the marginal contribution of real rates to return variation.

Full-sample evidence: Real rates as broad cross-asset headwind

Full sample results in Exhibit 4 indicate that increases in real interest rates are associated with negative return sensitivities for most major asset classes, highlighting the pervasive headwind imposed by rising real yields. Government bonds, credit assets, equities, and gold all exhibit negative real rate betas, while the US dollar stands out as a notable exception, displaying a positive and statistically significant relationship with real rates. This pattern is consistent with the view that higher real rates attract capital inflows and support currency appreciation.

Inflation expectations exhibit a positive and statistically significant association with most asset returns, consistent with recent evidence that increases in expected inflation — when interpreted as “good inflation” linked to stronger demand — compressed credit spreads and elevated equity valuations (Bonelli et al., 2025; Cieslak & Pflueger, 2023).14 This effect is absent for the USD and the JPY, where higher inflation expectations tend to weaken real exchange rate performance.

By contrast, consistent with the “fear‑gauge” framing of VIX in Whaley (2000)15 and the well‑documented inverse link between equity returns and implied‑volatility/VIX innovations (e.g., Giot, 2005; Dennis et al., 2006; Ding et al., 2021), our estimates show that the domestic risk assets are negatively exposed to both higher risk (VIX) and higher real rates, while positive VIX coefficients for the US dollar, MSCI ex‑US, and MSCI EM equities.

Taken together, the full sample evidence suggests that real rates already matter for asset returns when viewed over long horizons. However, these full-sample averages mask substantial time variation in the strength of real rate transmission, which becomes evident once the analysis is conditioned on regimes.

Regime-dependent effects: The post-QE re-pricing of real rate risk

The sub period analysis reveals a pronounced strengthening of real rate effects in the post QE environment as can be seen in Exhibit 5.1. During the pre QE and QE periods, equity returns display positive but generally insignificant sensitivity to real rate movements, reflecting an environment in which declining real yields, policy accommodation, and a high convenience yield muted the pricing of real rate risk.

In the post QE period, this relationship shifts decisively. Negative and statistically significant exposure of equity returns to real rate changes indicates that higher real yields now translate directly into lower equity returns.16 This pattern extends beyond public equities. Quarterly regressions show that private equity and private credit also exhibit negative and significant real rate sensitivities in the post QE period, suggesting that higher real rates now exert a direct drag on private market valuations (Exhibit 5.2). Similarly, global equities — including developed market ex US and emerging markets — display increasingly synchronized negative exposure to real rate shocks, pointing to a common transmission channel across regions.

The overarching implication is a regime shift in which real interest rates have transitioned from a background macro variable to a first order driver of cross asset returns.17

The negative real-rate betas in Exhibits 5.1 and 5.2 may appear difficult to reconcile with the strong headline performance of US equities, private assets, and gold post-QE period. The reconciliation rests on a fundamental distinction between marginal sensitivities and realized return outcomes. The estimated coefficients isolate the conditional response of asset returns to real-rate shocks, holding other macro drivers constant, rather than describing the unconditional return distribution, which also embeds earnings growth, fiscal stimulus, and geopolitical risk premia.

In that context, post-QE equity gains have been disproportionately concentrated in a narrow cohort of AI-exposed mega-cap firms, whose idiosyncratic earnings expansion and market dominance have driven index-level returns. The resulting concentration means that idiosyncratic growth dynamics have, at the aggregate level, more than offset the valuation headwinds associated with higher real discount rates, consistent with the mechanics of asset pricing whereby rising rates depress present values but need not dominate realized returns when cash-flow expectations shift materially.

Gold's resilience reflects a related but distinct mechanism. Its strength is better understood through the erosion of the convenience yield on traditional safe assets, alongside sustained central bank demand for reserve diversification amid geopolitical uncertainty, rather than as a contradiction of real-rate sensitivity. In this sense, gold’s performance is consistent with a reconfiguration of the safe-asset premium rather than a breakdown in the underlying transmission channel.

The post-QE coefficients should be interpreted as describing an underlying macros transmission mechanism, one that operates beneath headline return realizations and is partially masked by concentration effects in shifting risk premia. The breadth and persistence of these sensitivities, however, remain economically meaningful and provide the basis for the diversifier characteristics examined below.

The search for diversifiers

As real rates become a dominant pricing force, a natural question arises for asset allocators — Does meaningful diversification remain achievable? Sector and factor level results provide a nuanced answer.

At the sector level, cross sectional differentiation weakens in the post QE period (Exhibit 6.1). Most sectors exhibit negative or insignificant real rate sensitivities, implying that higher real rates operate primarily as a broad macro headwind rather than a sector specific pricing mechanism. Notable exceptions include energy, materials, utilities, consumer discretionary, and commodities, which retain either positive or less negative exposure and therefore preserve some hedging value when real rates rise.

Factor results point to a similar conclusion (Exhibit 6.2). Most equity and FX factors display limited and statistically insignificant sensitivity to real rate movements, suggesting that traditional factor premia are largely orthogonal to real rate shocks. However, equity value, FX carry, equity differential, and momentum factors consistently exhibit positive coefficients, supporting their role as partial structural diversifiers in a higher real rate regime.

Taken together, the evidence points to a materially more challenging environment for traditional multi asset portfolios. The broadening of negative real rate sensitivities across asset classes, combined with the rising explanatory power of real rates, implies reduced diversification benefits precisely when real yields are structurally higher. In this setting, portfolio construction must place greater emphasis on explicit real rate exposure management, selective use of sector and factor tilts, and a reassessment of assets historically treated as duration insensitive.

The following section translates these empirical findings into concrete implications for strategic asset allocation in a structurally higher real interest rate regime.

Implications for asset allocation

Our findings point to a structural shift in the real interest rate environment in the post QE period, with important implications for asset pricing and portfolio construction. Building on earlier evidence that rising public debt erodes the convenience yield of US Treasuries (Thiagarajan et al., 2025), the trend decomposition study indicates that this erosion is now transmitting into higher equilibrium real interest rates. As fiscal pressures persist, this channel suggests that upward pressure on trend real rates is unlikely to be easily reversed, marking a departure from the low real rate regime that prevailed during the QE era. In this context, real interest rates increasingly reflect fiscal and structural forces rather than cyclical normalization alone (Szoke et al., 2024; Jiang et al., 2024).

At the same time, asset returns have become more uniformly sensitive to movements in long tenor real rates. With the exception of the US dollar, increases in 10 year real yields exert a negative and statistically significant effect across major asset classes post QE. These results indicate that returns are increasingly driven by a common real interest rate factor, diminishing the diversification benefits historically associated with multi asset portfolios. As a result, traditional allocation frameworks that relied on offsetting responses (to rate shocks) across asset classes appear less effective, particularly during periods of tightening financial conditions.

In an environment of elevated and rising real interest rates, the similarity in directional responses across domestic and global assets underscores the need to reassess sources of diversification. Assets and strategies whose return profiles exhibit positive or weak sensitivity to real rate increases — such as the US dollar, energy equities, equity value strategies, and FX style premia including carry and momentum — may offer more resilient cushioning against real rate shocks. More broadly, these dynamics reinforce the importance of a regime aware approach to asset allocation, in which portfolio construction adapts to the evolving role of real interest rates as a dominant macro financial driver rather than relying on historical diversification patterns.

Conclusion

This paper addresses a question that sits at the core of today’s macro financial debate: whether the post pandemic rise in real interest rates reflects a temporary cyclical normalization or a more durable structural shift in equilibrium real yields. This distinction directly informs asset valuation, portfolio diversification, and the continued role of US Treasuries as the foundation of defensive asset allocation.

Our analysis provides consistent evidence that the recent increase in real interest rates represents a structural reconfiguration rather than a transitory policy effect. By extending the Del Negro et al. (2017) framework through the post QE period, we show that the dominant force behind the multi decade decline in real rates — the rising convenience yield on US Treasuries — has reversed. The erosion of both the safety and liquidity components of the convenience yield, alongside the reemergence of positive term premia, has mechanically lifted trend real rates. Importantly, this shift is closely linked to persistent fiscal deficits, rising Treasury supply, and deteriorating debt dynamics, suggesting that downward pressure on the convenience yield is unlikely to reverse quickly.

The asset pricing evidence reinforces this conclusion. Across regimes, real interest rates have transitioned from a secondary macro variable to a first order cross asset pricing factor in the post QE environment. With the exception of the US dollar and a narrow set of sectors and factors, higher real rates now exert a broadly negative and increasingly synchronized effect on returns across equities, credit, commodities, and private assets. Equities, which were largely insulated from real rate shocks during the QE era, now exhibit statistically significant negative exposure, materially weakening the diversification benefits that underpinned traditional 60/40 portfolio constructions.

For asset managers and asset owners, these findings carry several practical implications. First, reliance on long duration Treasuries as a standalone defensive hedge is increasingly fragile. While Treasuries remain indispensable for liquidity and collateral purposes, their ability to offset risk asset drawdowns has diminished in a regime of structurally higher real rates. Second, diversification must become more regime aware, with greater emphasis on assets and strategies that display resilience to real rate shocks, including safe haven currencies, energy linked assets, and select equity and FX style premia. Third, explicit management of real rate exposure — rather than implicit reliance on historical correlations — should play a more central role in strategic asset allocation frameworks.

More broadly, the results raise fundamental questions about how equilibrium real rates should be understood in an era of persistent fiscal expansion and declining safe asset scarcity. If the convenience yield on sovereign debt is no longer stable, then real interest rates may become more volatile, more regime dependent, and more tightly linked to fiscal credibility than in the past. In that world, diversification is no longer a structural property of portfolios but a conditional outcome, contingent on macro financial regimes. The central implication is that asset allocation can no longer treat real rates as a passive background variable; instead, real interest rates emerge as an active state variable that shapes correlations, hedging effectiveness, and the boundary between cyclical and structural risk.

Acknowledgements

The authors thank Michael Metcalfe, Jennifer Bender, David Turkington, Jiho Han, Elliot Hentov, Kamal Gupta, Eric Garulay, and Priyaam Roy for their invaluable contributions to the development of this paper. Their thoughtful critiques, constructive feedback and engaging discussions on earlier drafts significantly enriched the clarity, depth, and rigor of our work.