Insights

Navigating Europe’s shifting retirement landscape

Europe’s pension systems are facing structural pressure from demographic change, fiscal constraints, and shifting work patterns, requiring new, future‑ready retirement architecture.

March 2026

Denis Dollaku

Global Chief Executive Officer of State Street Bank International GmbH

Democratising financial security in retirement has been one of the greatest financial innovations of the last century. Today, retirement savings sit at the centre of the global financial system, and Europe’s pension systems enable hundreds of millions of citizens to make provision for later life.

However, our latest report, The shifting global landscape for retirement, reveals how several structural forces are causing countries around the world to confront the resilience of their pension systems. In this rapidly changing environment, success no longer comes just from picking the right fund. The challenge now lies in developing future-ready architecture. Our ability to design systems that will sustain people in a dignified and secure retirement for decades to come is what’s truly at stake.

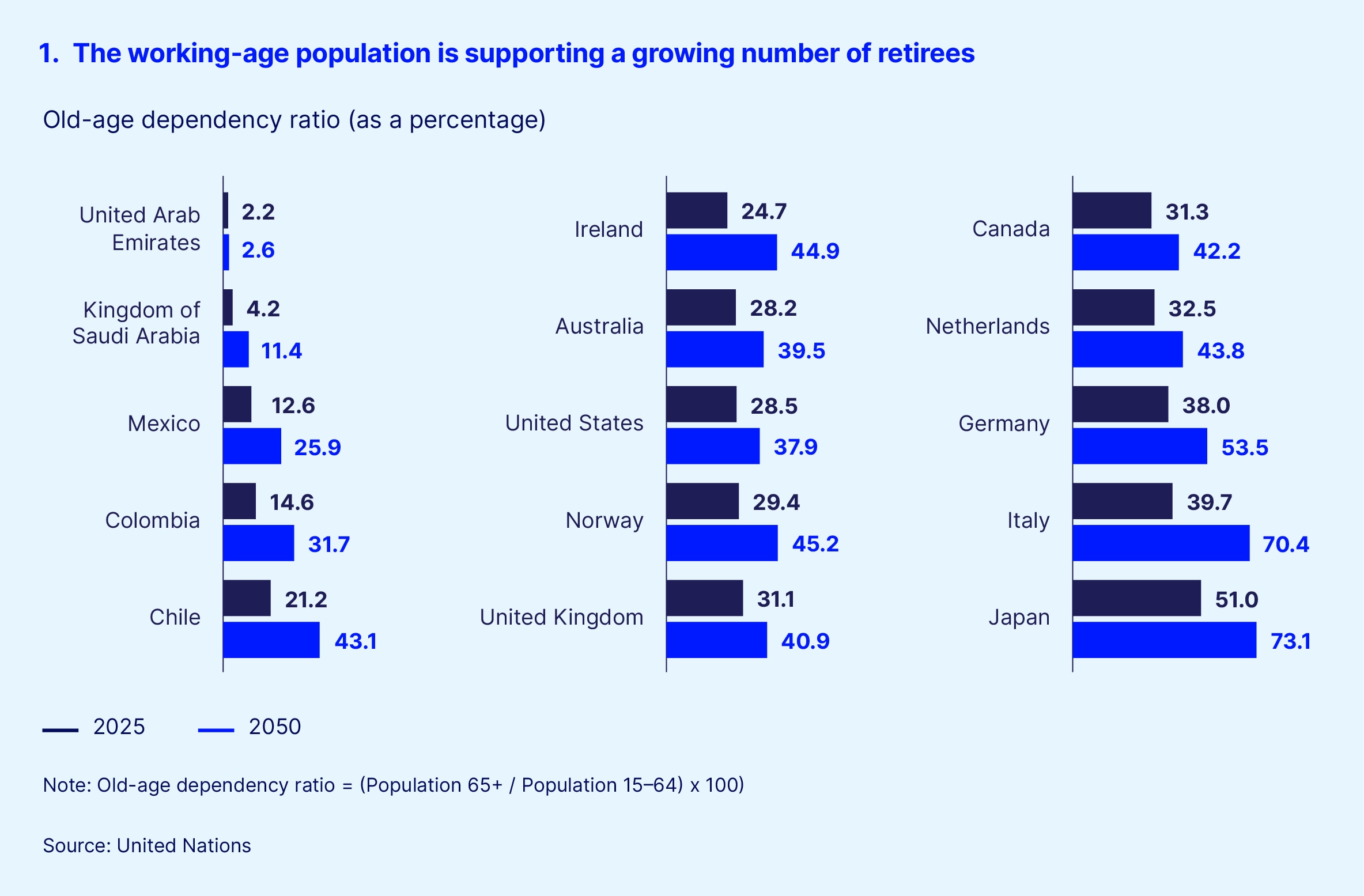

Exhibit 1

Understanding the global forces at work

Europe’s retirement map: Three starting points, one destination

To understand how these trends affect retirement systems in Europe, one must first recognise that the continent is not a monolith. European countries are approaching this transition from very different starting points. In broad terms, there are three distinct pension models in Europe.

The first is the Bismarckian system, found in multiple countries, including Germany, Italy, and France. This is a state-led, pay-as-you-go model where today's workers fund today's retirees. This system is built on a generational promise: Your contributions today secure your parents' retirement, and the next generation will do the same for you. However, that promise is being stretched to its limit as the number of workers per retiree shrinks, forcing these countries to look beyond the state to fill the gap.

The second is the Anglo-American model, seen in the United Kingdom and Ireland. This system relies more heavily on voluntary private savings and defined contribution (DC) plans. While fiscally resilient, it faces a significant adequacy gap, as the burden of saving (and the risk of market volatility) sits squarely on the individual's shoulders.

The third is the Advanced Multi-Pillar model, championed by the Netherlands, Norway, and Iceland, who have some of the most sophisticated systems in the world. This model combines high trust, collective risk-sharing, and mandatory funded pillars.

While these three archetypes represent different starting points, the three systems are converging as every European system is attempting to solve the same set of challenges.

The forces of change

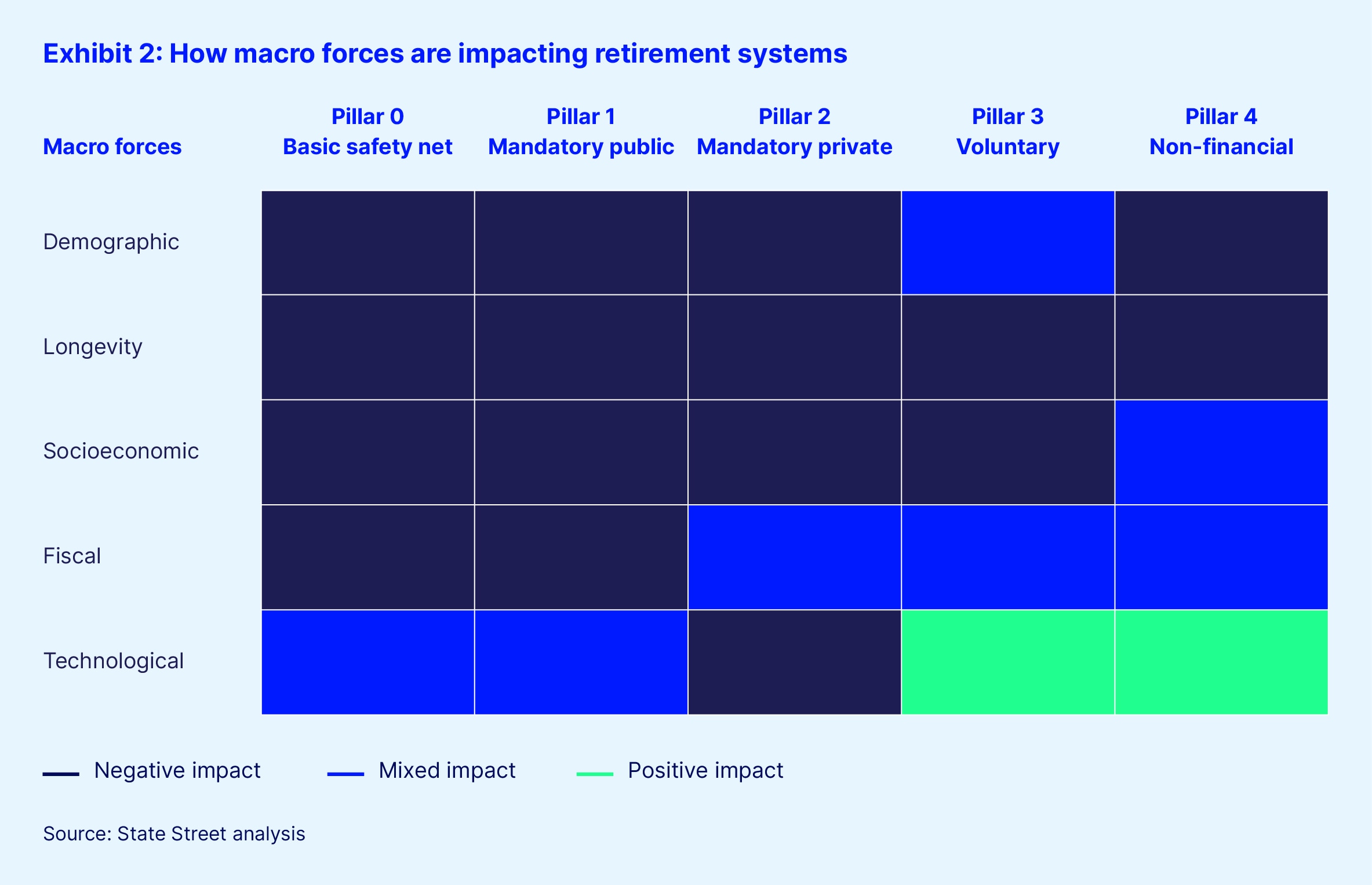

What is driving this convergence? It is not a single event, but a set of system-wide stresses generated by five persistent macro forces that have narrowed the policy space for European governments.

First, a demographic squeeze. The working-age population is shrinking just as the number of retirees expands.

Second, rising longevity. Longer lifespans are a triumph for modern medicine, but they also contribute to decumulation risk — the very real danger that many citizens will outlive their assets.

Third, changing work patterns. The socioeconomic shift toward gig and platform work means fewer people are tied to traditional, long-tenure careers with built-in employer pensions.

Fourth, fiscal constraints. High public debt and higher real interest rates mean governments can no longer afford to fill the gap.

Finally, technological acceleration. Technology is both a threat and a tool, demanding the full digitisation of the retirement experience.

Combined, these forces are shifting the burden of risk from the state to the individual. In this individual-centric era, the old products aren't enough. We need new architecture that is inclusive, resilient, and digitally integrated enough to deliver the secure financial future that Europe’s citizens deserve.

Six value pools for a new era

This is the heart of the European opportunity. As systems are converging, six distinct value pools emerge where innovation is not just possible for the industry, but mandatory.

1. Solving the decumulation challenge

For 30 years, the industry’s focus was accumulation — in other words, how to help people save. Now, we face a harder challenge known as decumulation, or how to turn these savings into predictable income flows for the rest of retirees’ lives.

In the Netherlands, the landmark Wet toekomst pensioenen (WTP) reform is the global test case. As the system transitions €1.8 trillion into individual accounts, it is introducing default income pathways. Here, the system’s architecture creates the equivalent of a predictable paycheck, using collective solidarity reserves to smooth market shocks so a retiree’s income doesn't vanish during a downturn.

2. Digital dashboards

In Europe, fragmentation is a major obstacle to retirement security, with billions of euros currently sitting in "lost" pension pots. In the UK alone, there are an estimated 3.3 million lost pots worth over £31 billion. To address this, Europe is leading the adoption of national dashboards that aggregate lifetime savings data into a single, unified view for the individual.

Norway’s Egen Pensjonskonto (EPK) system and Germany’s Digitale Rentenübersicht are turning this raw data into a strategic distribution asset. In Germany, the national dashboard already aggregates roughly 137 million records from more than 700 providers. When citizens can see their entire retirement history in one mobile-friendly interface, engagement skyrockets.

For financial institutions, being "dashboard-ready" becomes vital. If your architecture cannot integrate data into these systems via secure application programming interfaces (APIs), you effectively become invisible to the consumer.

3. The portable account

The traditional employer-centric pension is failing the modern, mobile workforce. Success now requires an individual-centric design.

Ireland’s launch of national auto-enrolment in 2026 is the blueprint. It brings 800,000 previously unpensioned workers into a system where the account follows the worker. Whether you are a gig worker in Dublin or a tech consultant moving across the European Union, your retirement savings stay with you. This portability is the only way to ensure adequacy for a 21st-century labour market.

4. Institutional risk transfer

Higher interest rates have opened a window of opportunity for corporate sponsors. Many legacy defined benefit plans are now well-funded for the first time in years.

In the UK and Ireland, companies are rushing toward the endgame, paying life insurers to take these liabilities permanently off their balance sheets through bulk purchase annuities (BPAs). This creates a massive new class of asset owners who need industrial-scale custody and in-kind asset transfers, where the underlying securities are handed over directly to the insurer rather than being sold for cash. It marks the final transition of pension risk from the corporate world to the insurance world.

5. Solving the liquidity paradox

As pension funds consolidate into mega-funds, such as the Dutch Pensioenfonds Zorg en Welzijn (PFZW) or UK Master Trusts, they face a liquidity paradox. These entities are becoming too large for public stock markets to absorb their capital without distorting prices.

To find returns, scale capital is rotating into private markets. Driven by policy shifts like the Mansion House Accord in the UK, funds are allocating billions to private infrastructure, credit, and green energy. These real assets provide the long-term, inflation-linked cash flows that retirees need. However, managing private markets at scale will require far greater data transparency, valuation discipline, and operational sophistication.

6. Women and the “Great Wealth Transfer”

The final value pool is about extending security to people that the system has historically left behind. The EU’s 29 percent gender pension gap is a structural failure that punishes caregiving and career breaks. At the same time, a generational shift is underway: The "Great Wealth Transfer" is moving trillions of euros into the hands of younger, digital-native cohorts who view retirement differently.

These new wealth-holders demand more than simple returns. Many of them want their capital to help fund the transition to a net-zero economy. For providers, sustainability is no longer an optional ESG checkbox — it is a core requirement for doing business in the modern European market.

Architecture for the future of retirement

The social contract that has underpinned retirement systems in Europe for over 100 years must evolve. In the 20th century, there was an implicit agreement where the state or employer guaranteed security in exchange for a lifetime's commitment from the worker. Today, that contract is being rewritten as a partnership where the individual holds the risk, but the industry provides the architecture to manage it.

For asset managers, the era of simple asset gathering is being replaced by an era of outcome delivery. The goal is no longer just to build a pot of wealth, but to provide the predictable paycheck that the state can no longer guarantee on its own.

Asset owners and pension trustees will need new capabilities and systems. The complexity of managing private markets, integrating with national dashboards, and meeting shifting regulatory mandates requires a robust digital foundation. In this new landscape, trust in the system is sustained not just by investment returns, but by the transparency and reliability of your systems and operations.

We are at a strategic inflection point in the pension industry. By focusing on these six value pools and modernising the underlying architecture, we can ensure that the retirement system remains a pillar of global financial stability and a steadfast source of security for the billions of people who rely on it.

Discover how our European market solutions can help you elevate your strategy, unlock insights, drive growth, and stay ahead.