Insights

November 2025

Compelling forces in the democratization of private markets

Industry expectations for the adoption of retail-style private markets funds have surged faster than anticipated.

Susan Doyle

Global Head of Private Markets Funds, State Street Investment Management

Stephen Martin

Head of Asset Backed Securities, Challenger Investment Management

John Gee-Grant

Global Head of Client Solutions, IFM Investors

Peter Beske Nielsen

Global Head of Private Wealth & Evergreen Solutions, EQT Partners

Kira Mikulecky

Principal, Deloitte

Gautham Ratnakar

Financial Markets Infrastructure,

Alvarez & Marsal

William Sammons

Wealth & Asset Management,

Alvarez & Marsal

James Redgrave

Vice President of Global Thought Leadership,

State Street

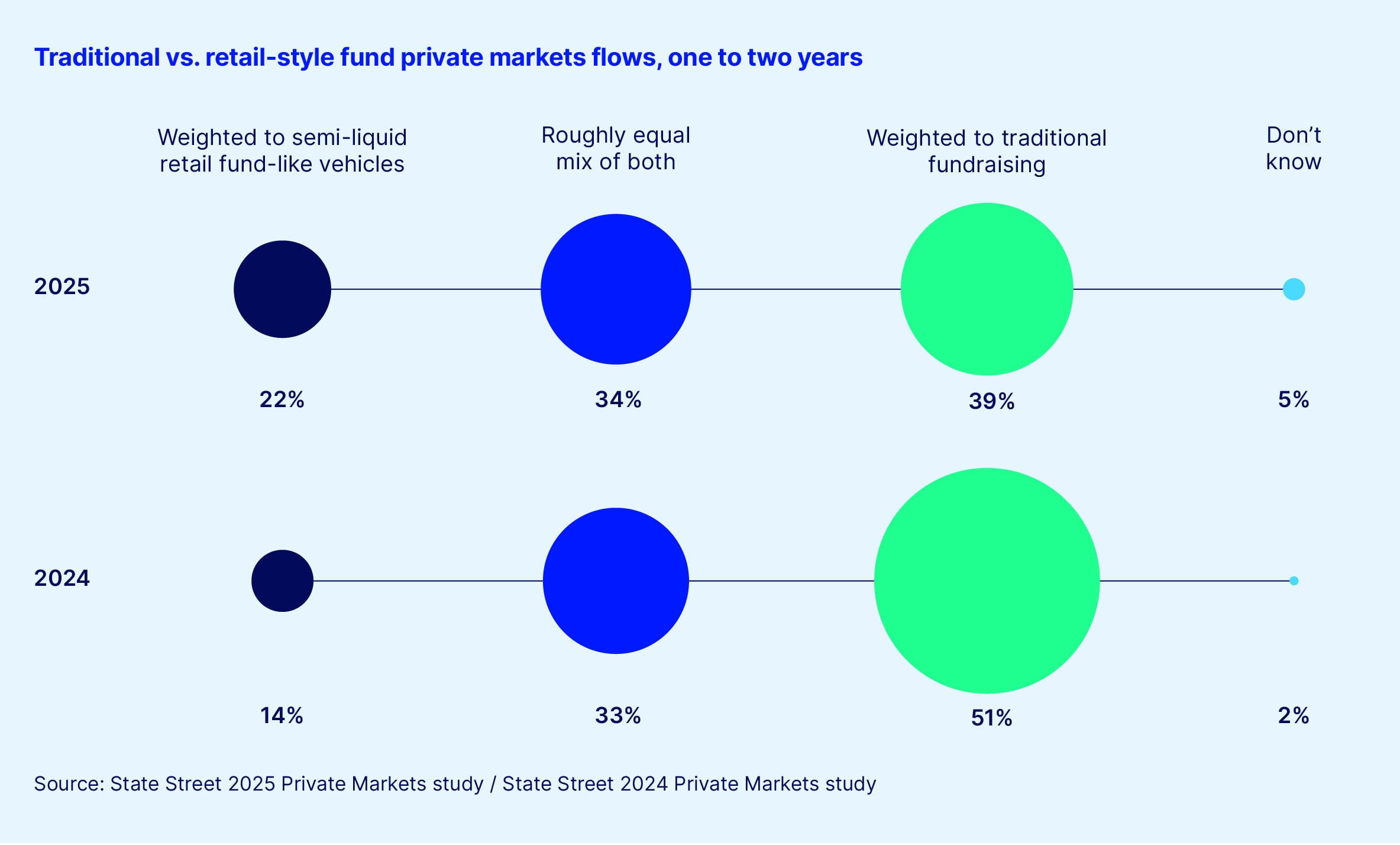

Earlier this year, we released Driving success in volatile environments, our whitepaper based on insights from the 2025 State Street Private Markets Study. In the paper, we highlighted a striking trend: The industry’s expectations for the adoption of retail-style private markets funds had accelerated faster than anyone anticipated.

This finding represents a departure from our 2024 study, in which responses from nearly 500 executives at limited and general partners (LPs and GPs) around the world pointed to steady, gradual growth for retail-style private markets products. Clearly, those same voices anticipate a far more rapid trajectory today.

Specifically, between the two pieces of research, the number of respondents who believed the majority of all flows would come through individual investor-focused funds within two years grew from 14 percent to 22 percent, while the number who thought traditional fundraising would continue to dominate fell from 51 percent to 39 percent, as shown in Figure 1. Additionally, more than half (56 percent) thought retail-style funds would account for at least half, if not the majority of flows in two years’ time.

To further explore this dramatic shift, we convened a panel of leading experts from asset management, institutional asset ownership and consultancy. The panel discussion explored what’s driving this rapid growth and examined what it means for the future of the investment and savings industry.

Missed the first installment in the series?

Global institutional investors are rapidly evolving their strategies to seize new opportunities in today’s dynamic markets. Download our latest report to discover how industry leaders are tapping into fast-growing private markets to boost growth.