The shifting global landscape for retirement

What's inside

Retirement is no longer a static, end-of-career event. It is a system-level challenge that affects billions of people and sits at the center of global capital markets.

Across regions, retirement systems are at an inflection point — more people are entering retirement while living longer in retirement at a time when real rates and equity valuations are high and government funding limited. These structural forces are not just reshaping retirement systems, but individual retirement outcomes and the commercial landscape for providers.

To understand how demand for retirement-related financial services is changing as a result of these structural forces, we connect macro to micro analysis, and identify where financial services could meet this shifting demand.

We start with five global forces — demographic, health and longevity, socioeconomic, fiscal, and technological — and map their directional impact across the World Bank’s multi pillar retirement architecture. We apply that cross-pillar lens to a diverse set of 15 countries, connecting system design to real operating decisions across the retirement ecosystem (e.g., sponsors, advisors, asset managers, administrators and recordkeepers, custodians, regulators and supervisory authorities, and participants). Key findings include:

Retirement is being redefined at the system level: Focus shifts from saving to outcomes

Despite wide variation in history and structure, retirement systems globally face a shared challenge: balancing fiscal sustainability with adequacy, portability and confidence over longer lives. Longevity no longer simply extends retirement; it reshapes the boundary between work and retirement itself. As careers become less linear and life expectancy rises, systems must support flexible transitions, manage risk over longer horizons and deliver dependable income rather than focus solely on asset accumulation.

This reflects a shift from accumulation alone toward delivered outcomes. Retirement success is being defined not by balances at retirement, but by the system’s ability to convert savings into sustainable income, manage risk explicitly and anchor confidence through governance and execution.

While there are inherent differences among retirement systems, they are converging around similar pressure points

Comparative analysis across retirement system models shows convergence toward shared priorities, even as national designs differ. Systems face similar design questions around income delivery, risk sharing, coverage and execution:

- Anglo-American systems (US, UK, Ireland) remain fiscally resilient but face adequacy gaps driven by reliance on funded pillars. Expanding coverage through auto-enrollment, nudges and portability is pivotal, alongside longer working lives.

- Bismarckian systems (Germany, Italy, Japan) confront acute demographic strain in pay-as-you-go structures. Reform paths shift more risk to individuals, elevating the importance of lifetime income design and decumulation defaults.

- Advanced multi-pillar systems (Netherlands, Norway, Canada, Australia) show greater diversification and resilience, yet face complex transitions — including collective DC migration — and the need to extend coverage to self-employed workers.

- Latin-American systems (Chile, Colombia, Mexico) are rebalancing individual account models toward multi-pillar designs to improve adequacy and equity amid labor market informality.

- Gulf systems (UAE, KSA) are modernizing citizen pensions and expatriate benefits as demographic change, fiscal diversification and decarbonization reshape long-term sustainability.

Architecture, not products, is determining the resiliency of retirement systems

Across markets, system architecture — rather than any single product — is becoming the primary determinant of retirement outcomes. The systems proving most resilient share common characteristics: they coordinate effectively across pillars, make risk-sharing explicit, design for decumulation early, and use governance, transparency and execution discipline to anchor trust.

Shifting demand is creating opportunities for financial services

Several value pools (opportunities for economic profit and outcome improvement) are emerging where system pressure is concentrating:

1. Decumulation and retirement income are becoming the defining frontier. As large defined contribution (DC) cohorts retire, systems are standardizing default income pathways that blend guided drawdown, risk pooling and where appropriate annuitization. These shifts elevate income sustainability, not balances, as the primary outcome.

2. Digital engagement and hybrid advice are turning data into action. National dashboards and integrated platforms are consolidating records and orchestrating next-step decisions. Secure data sharing, behavioral design and cyber-resilient workflows are central to execution.

3. Coverage expansion and portability are unlocking new contributors and assets. Auto-enrollment, low-friction onboarding and portable accounts are extending funded systems to previously excluded workers and reducing leakage over working lives.

4. Defined benefit (DB) risk transfer solutions are scaling. High funding ratios are accelerating bulk annuity and longevity solutions, making execution capability — data readiness, member communication and liability-aware portfolio construction — a strategic differentiator.

5. Scale capital is rotating toward private markets as governance expectations rise. Retirement systems seek diversification, inflation linkage and long-duration returns, while sustainability considerations increasingly shape how capital is governed and allocated.

6. Women and younger cohorts are emerging as cross-cutting demand drivers. Intergenerational wealth transfer and digital-first engagement are reshaping income design, experience delivery and system expectations. These shifts are structural, not cyclical.

Taken together, these findings underscore a clear conclusion: Retirement outcomes are increasingly shaped by system design, governance and execution — not by isolated products or point solutions. As demographic, policy and capital-market pressures converge, institutions that can coordinate architecture, advice and execution at scale will be better positioned to deliver durable income, manage risk and sustain trust over time.

A global architecture for retirement

Around the world, retirement systems reflect a patchwork of approaches to funding, risk-sharing and governance, underscoring the widespread demand for financial services to support people’s lifestyles and goals as they leave the workforce. Global trends and economic linkages are shaping the supply and demand of capital and liquidity for current and future retirees — and those dynamics are in flux.

To understand this vast yet intricate picture, we begin with a framework of the key macro forces reshaping retirement systems around the world and lay out our methodology for analyzing the impacts of these forces. Next, we evaluate the effects on comparative retirement systems. Finally, we lay out an ecosystem view to identify both the stakeholders affected and opportunities emerging for the financial services industry.

Our country sample

While the macro forces we identify in our analysis are global, their impact crucially depends on the design of national retirement systems. We have chosen a sample of 15 countries from three major regions: the Americas, APAC, and EU plus broader regions. Within these regions, we selected a diverse mix of nine mature economies including the US, Canada, Japan, Australia, the UK, Ireland, Germany, Italy, the Netherlands, and Norway. In addition, we picked five emerging economies from Central and South America including Chile, Mexico, and Colombia as well as two from the Middle East, the UAE, and the KSA to round out our regional view.

Five forces reshaping the retirement landscape

There are myriad macro forces at work today that are impacting retirement systems in some way. These include changing demographics, longevity and health trends, the nature of work, widening income gaps, rising health care and housing costs, government debt, technological innovation, shifting economic fundamentals, and financial asset performance.

To examine which of these are most relevant, we draw on State Street’s economic analysis, which identifies five key forces reshaping the global economy.1 These forces are persistent and observable drivers of retirement system change across markets, informed by long-term monitoring of demographic, fiscal, technological and labor market trends.

Applied to retirement, they define the main categories of macro forces impacting retirement systems:

1. Demographic: Including aging demographics and evolving social structures

2. Health and Longevity: Including longevity, wellness and long-term care

3. Socioeconomic: Including the future of work and growing inequality

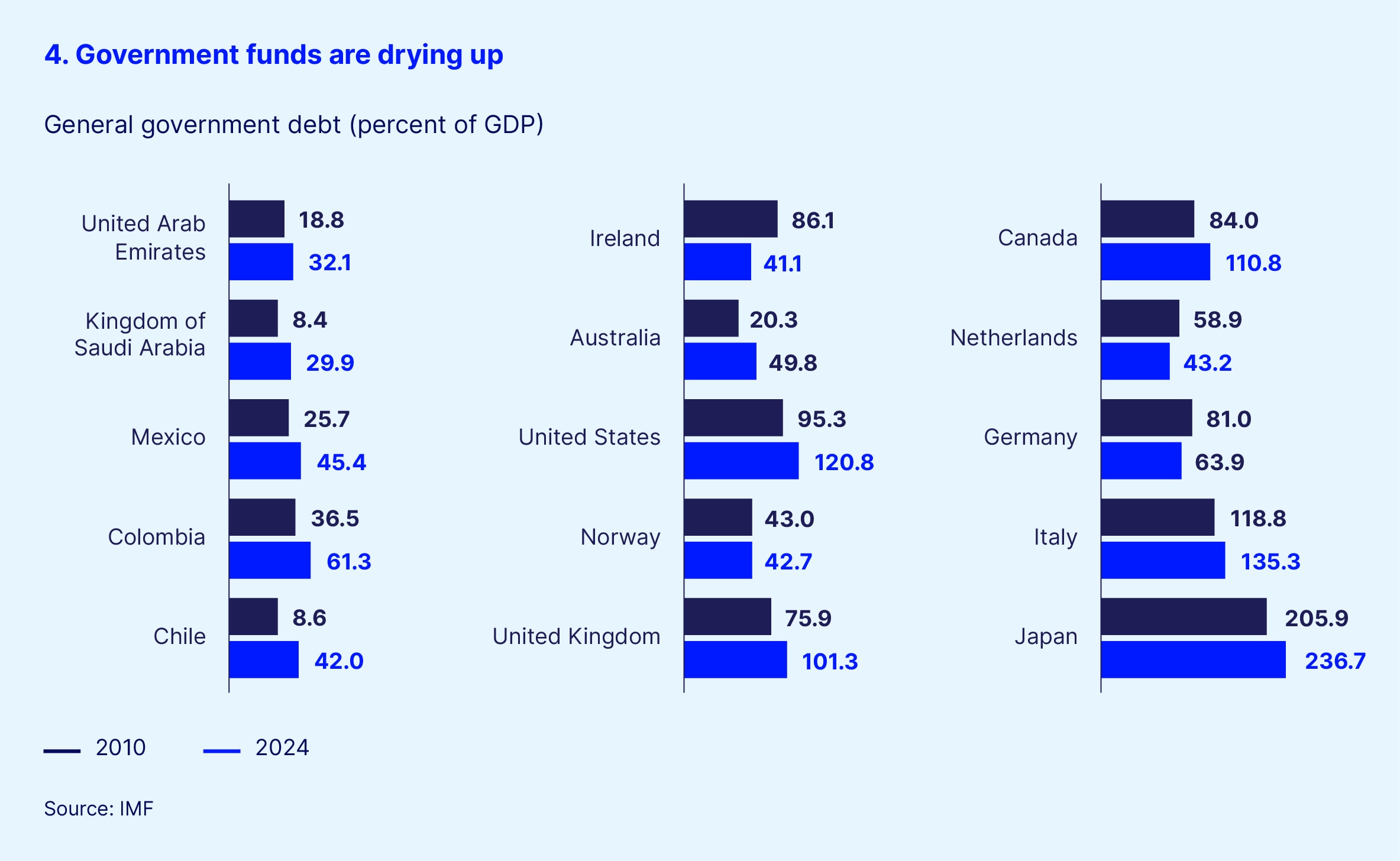

4. Fiscal: Including rising sovereign debt and higher real interest rates

5. Technological: Including automation, digitization and fintech

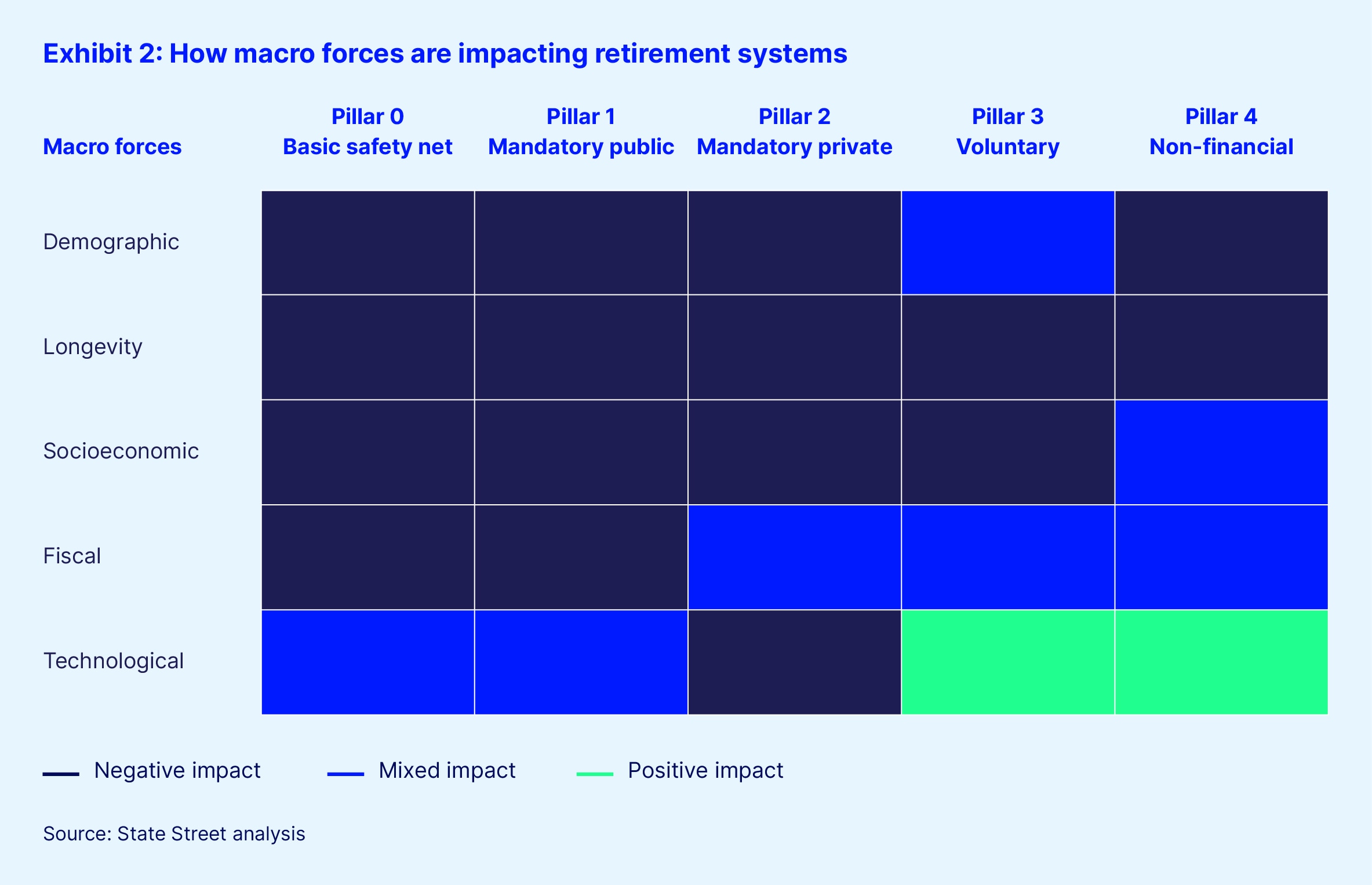

These five macro forces capture the dominant, system-wide shocks to different retirement architectures (see Exhibit 1).

Exhibit 1

Understanding the global forces at work

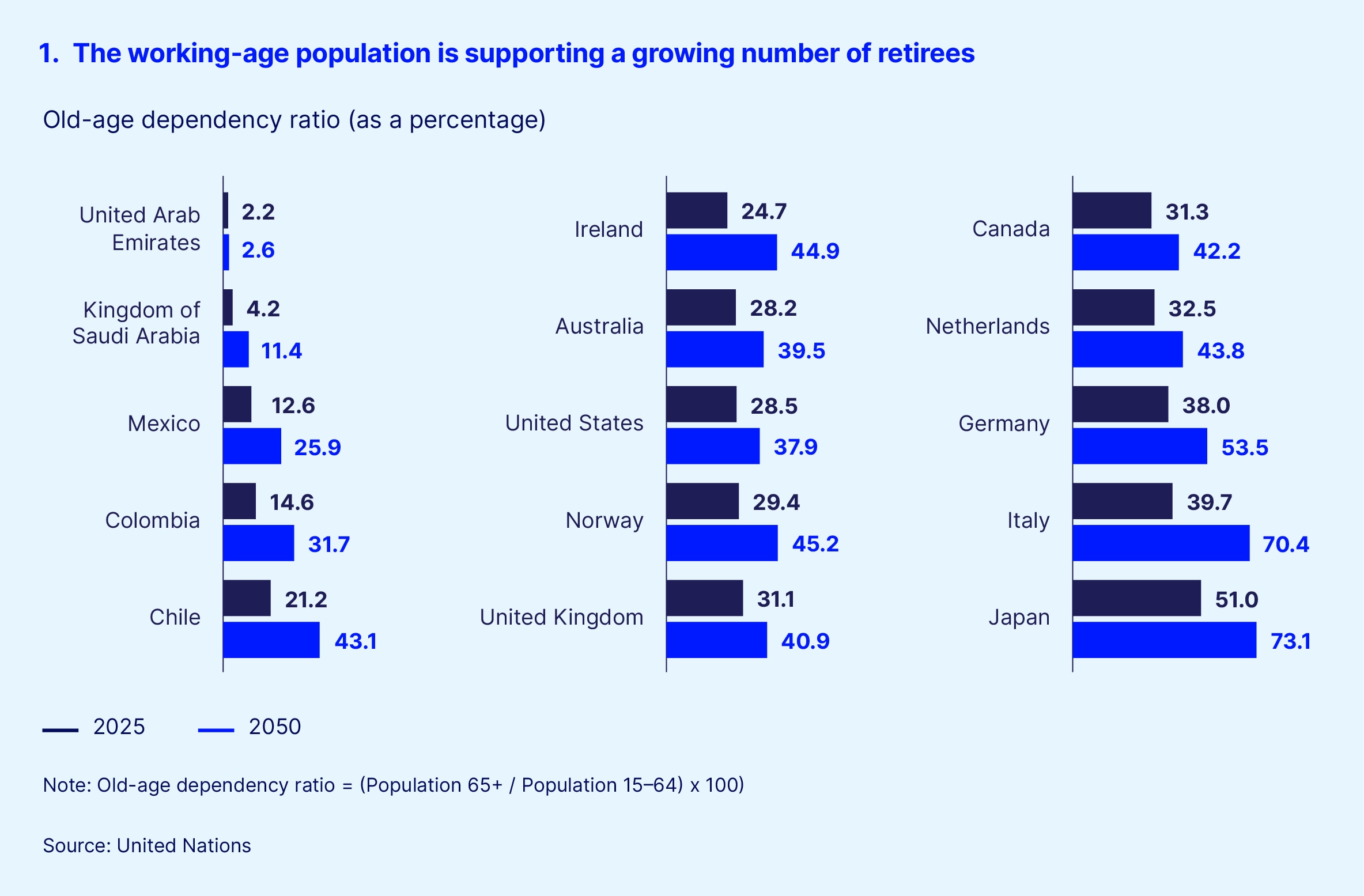

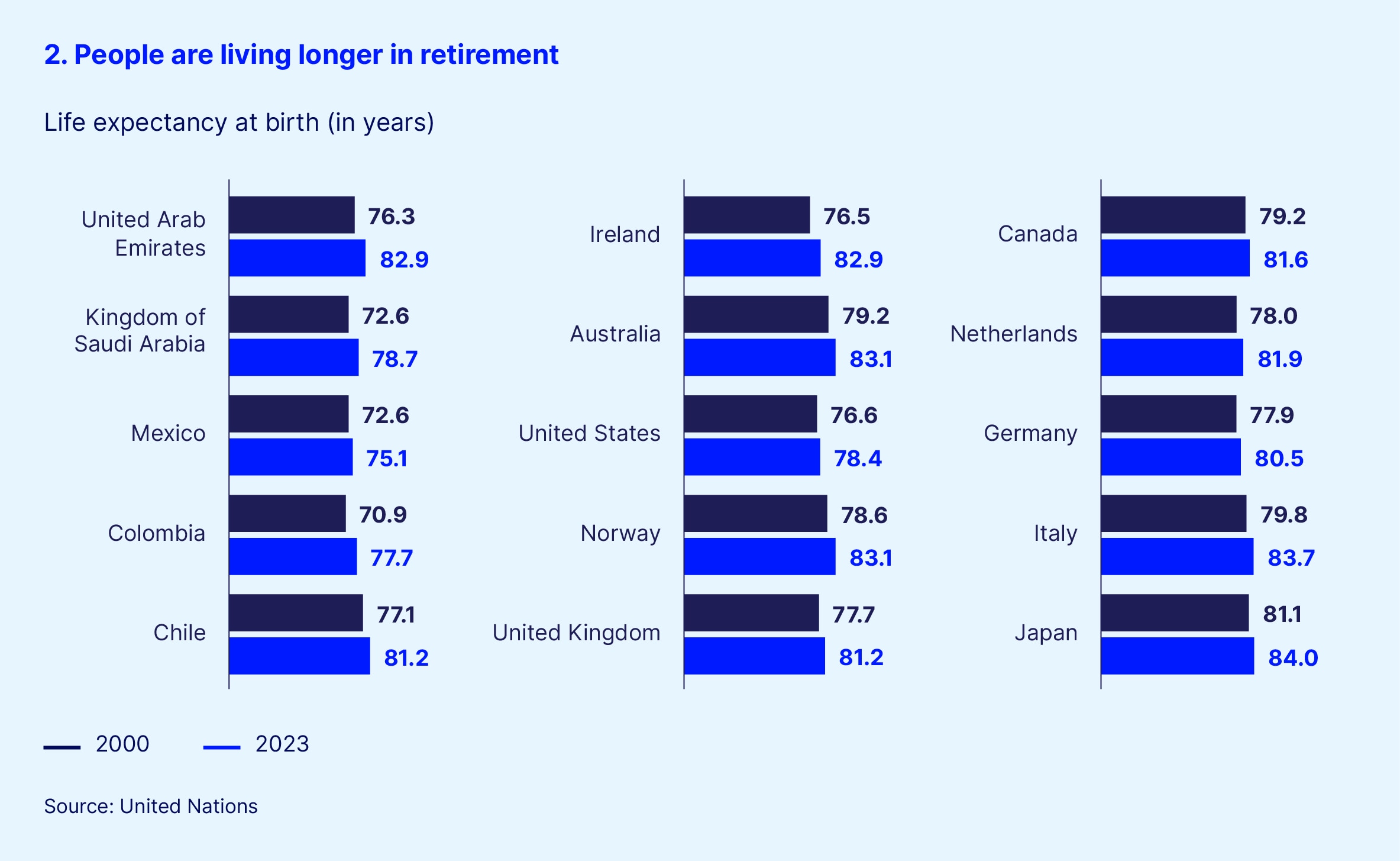

Demographic aging reduces the relative size of prime-age workforces in many regions while expanding the population that must rely on saved assets and public transfers. Longevity extends retirement horizons, magnifying decumulation risk and placing sustained pressure on PAYG systems as worker-to-retiree ratios decline. However, rising life expectancy does not imply a fixed or uniform retirement boundary. Across advanced and emerging economies alike, healthier aging and evolving labor markets are gradually extending working lives through later-career participation, phased retirement and non-traditional employment. As a result, retirement sustainability is increasingly shaped not only by population aging, but by the degree to which systems support longer, more flexible transitions between work and retirement.

Health and longevity trends amplify retirement system pressure by extending benefit durations and increasing exposures to healthcare and long-term care costs. Longer lives raise the risk of outliving assets, intensify decumulation challenges and increase the fiscal burden on systems where longevity risk is not pooled. The net impact depends on whether retirement architectures and labor markets are designed to accommodate later-life work. Where systems remain ridged, rising longevity magnifies solvency risk and shifts greater responsibility onto individuals, families, employers and public finances.

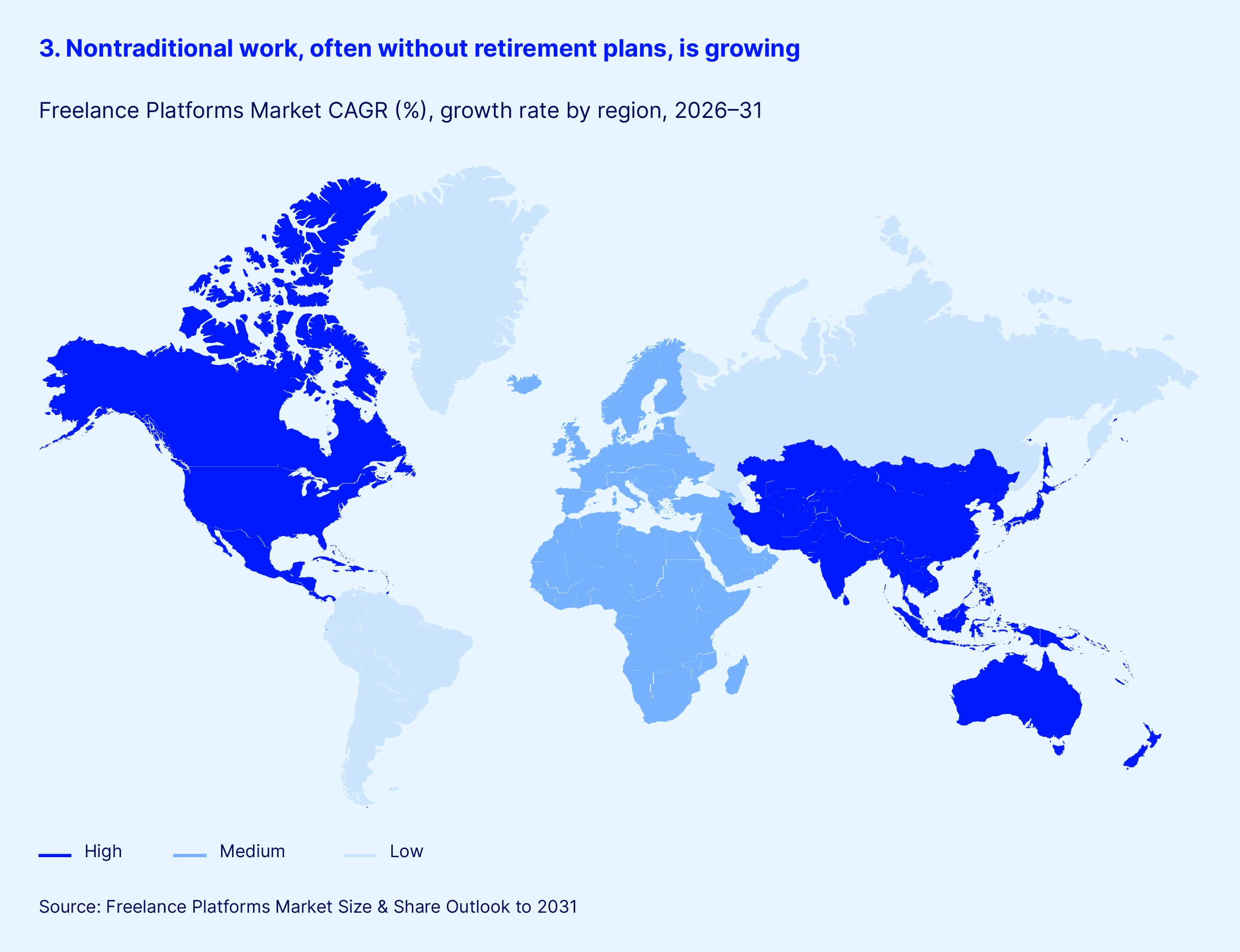

In parallel, socioeconomic change weakens the standard employment relationship through more frequent job switching, incomplete benefits coverage, and the rise of gig and platform work that strains systems designed around stable, long-tenure careers. Higher public debt and higher-rate environments raise debt-servicing burdens and narrow policy space that may lead to recalibration of retirement programs through eligibility, indexation, or benefit design. Furthermore, persistently higher inflation — especially in services such as housing and healthcare — directly erodes the purchasing power of aging households and necessitates inflation-resilient income pathways. Technological transformation compounds these shifts in positive and negative ways.

Automation and digitization could lift productivity and enable more personalized financial intermediation, yet they concurrently reshape labor demand and widen dispersion in lifetime earnings. Together, these dynamics are reshaping how risk is allocated across states, employers, markets, families and individuals.

In order to determine the impact of these five forces on different retirement systems, we categorized each retirement system according to the World Bank’s multi-pillar framework:2

Pillar 0 (Basic Safety Net) provides baseline economic support, typically funded through general taxation and targeted through means-testing to reduce old-age poverty.

Pillar 1 (Mandatory Public Pension) consists of mandatory, publicly managed pensions financed through PAYG arrangements.

Pillar 2 (Mandatory Private Pension) comprises mandatory or quasi mandatory, employer- or institution-managed, privately funded pension plans financed by employer/employee contributions.

Pillar 3 (Voluntary Savings) includes voluntary individual retirement accounts and other self-directed savings vehicles.

Pillar 4 (Informal Support) encompasses informal mechanisms such as family care, intergenerational support and access to community or household resources.

While the same macro forces act across all pillars, their effects differ materially depending on funding structure, governance and where financial and longevity risk ultimately sits. We determined the direction of impact (positive, negative or mixed) of each of our five macro forces on each retirement system pillar (see Exhibit 2). And we use this cross-pillar impact analysis to determine how each one of our 15 country retirement systems is being impacted. (The results of our cross-pillar impact analysis by country can be found in the section “Country System Profiles”).

Broadly speaking, Pillar 0 (Basic Safety Net), which provides social assistance, faces growing pressure from demographic and longevity trends. As populations age, more individuals lack family support and rely on state-financed pensions for longer periods. Socioeconomic changes — especially the rise of gig and informal work — leave many older adults without contributory benefits, increasing demand for assistance. Technological change has mixed implications: Automation may weaken tax bases and displace workers, increasing need for support, while productivity gains from AI could strengthen public finances. Longevity amplifies fiscal pressure by lengthening benefit periods and increasing healthcare needs among the old. Fiscal conditions are a major constraint, as economic downturns or shifting policy priorities can undermine the adequacy or sustainability of Pillar 0 benefits.

Pillar 1 (Mandatory Public Pension), which encompasses public contributory systems, is increasingly strained by demographic shifts. Lower worker-to-retiree ratios and longer life expectancy reduce contributions relative to payouts, challenging PAYG models. Socioeconomic trends — such as irregular employment patterns, under-reported earnings in gig work, and wage polarization — further weaken contribution inflows while increasing the share of beneficiaries needing minimum benefits. Technological change brings mixed effects: Job automation may reduce contributors but can also create new, higher-wage roles, while digital tools can improve administrative efficiency. Rising longevity exacerbates solvency pressures by extending the number of benefit years and increasing disability-related claims among the population’s eldest. Fiscal stress heightens political risk, as financially constrained governments may adjust indexation formulas or pursue benefit reforms in response to rising debt and pension spending.

Although Pillar 2 systems (Mandatory Private Pension), which include mandatory occupational and employer-based plans, are less exposed to demographic financing imbalances than PAYG systems, they are still indirectly affected by aging societies through lower workforce participation and weaker asset growth in low-growth economies. Socioeconomic shifts — particularly the decline of traditional salaried roles and the rise of freelance or contract work — reduce enrollment and contribution consistency, undermining long-term asset accumulation. Technological change often has a negative impact when it accelerates industry disruption, leaving certain sectoral pension funds underfunded; however, innovation can modestly improve coverage and reduce administrative costs. Longevity increases the risk of outliving savings, particularly in DC schemes where individuals bear most of the risk, and also complicates annuity pricing. Fiscal trends have mixed implications: Higher interest rates can improve DB funding ratios and expected returns but may also prompt governments to reconsider tax incentives or shift public-sector DB plans toward more fiscally sustainable structures.

In the case of Pillar 3 (Voluntary Savings), which captures voluntary personal savings, demographic change may motivate greater personal saving, but behavioral biases such as inertia and short-termism limit actual participation. Socioeconomic factors — including income volatility and the financial fragility common among gig workers — tend to depress voluntary saving unless supported by nudging or automation. Technology is a strong positive force: fintech platforms, robo-advisors, digital literacy tools and automated saving mechanisms expand access and improve user engagement. Observed outcomes across markets show that voluntary systems face participation and adequacy gaps driven by behavioral frictions, income volatility and confidence — reinforcing the limits of reliance on Pillar 3 alone. Nonetheless, rising longevity exposes a persistent gap between what individuals save and what they will need, especially given rising medical and long-term care costs late in life. Fiscal conditions cut both ways. Higher real yields make saving more attractive, yet governments may face pressure to scale back tax incentives even as they rely on voluntary savings to reduce future burdens on public systems.

Lastly, Pillar 4 (Informal Support), which captures family and informal support, is negatively impacted by demographic trends. Smaller families, higher rates of single living and geographic dispersion reduce the availability of caregivers, increasing reliance on paid or institutional care. Socioeconomic changes have mixed effects. Some households may provide more support due to longer working lives or diversified income streams, while others face greater financial strain that limits their ability to assist older relatives. Technology generally strengthens Pillar 4 by enabling independent living through assistive devices, telemedicine, remote monitoring and flexible work opportunities that allow older adults to remain economically active. However, longevity intensifies the burden as the number of elderly grows while the pool of potential caregivers shrinks. Fiscal tightening compounds these pressures by reducing public spending on health, long-term care and social services, shifting responsibility back to families.

The impact on comparative retirement systems

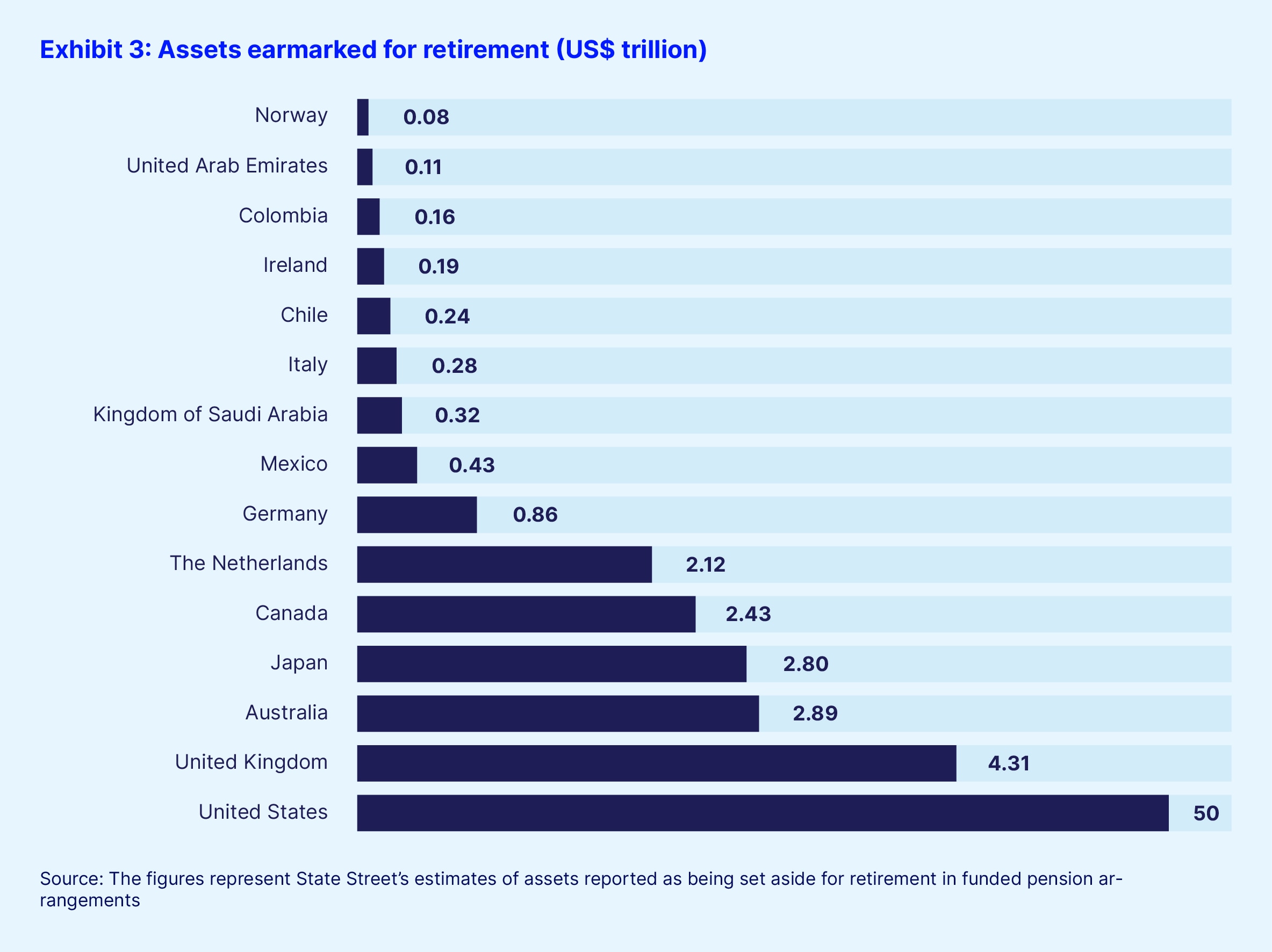

Across advanced and emerging economies, retirement systems reflect many differences from size to deeply rooted institutional traditions, labor market structures and demographic pressures, yielding distinct models with differing strengths and vulnerabilities (see Exhibit 3).

However, retirement systems can be grouped into a number of archetypes or models based on which institutional channels do the core work of retirement provision and how they allocate risk. Using the World Bank’s multi-pillar system (Pillar 0: Basic Safety Net, Pillar 1: Mandatory Public Pension, Pillar 2: Mandatory Private Pension, Pillar 3: Voluntary Savings, Pillar 4: Informal Support), different retirement systems can be classified by the pillars that are dominant in shaping (i) the financing of liabilities and fiscal exposure (sustainability), (ii) the primary sources of income replacement and poverty prevention (adequacy), and (iii) the breadth and continuity of participation across the life cycle (coverage). This, in turn, focuses attention on three core design questions: how retirement income is financed; how participation is achieved — through mandates, subsidies or behavioral nudges; and whether longevity, inflation and market risks are pooled collectively or borne by individuals.

We group our sample of 15 countries into five distinct models:

The Anglo-American model: This grouping includes the US, UK and Ireland, and emphasizes a modest public floor (Pillar 0/1) placing substantial weight on voluntary or quasi-mandatory funded pillars to deliver retirement adequacy. While this approach is fiscally resilient due to comparatively low public pension obligations, it is notably exposed to adequacy gaps, especially for workers with inconsistent or limited private savings. The rise of gig and nonstandard work further enlarges this at-risk group.

The Classic Bismarckian model: This includes Germany, Japan and Italy, and relies on large earnings-related public schemes (Pillar 1), typically delivering broad formal-sector coverage and comparatively stable replacement for full careers, but concentrating solvency exposure in the PAYG core. These systems are facing acute strain from demographic aging, with very low fertility and high longevity threatening system solvency. Structural reforms — including Italy’s shift to a national DC framework and Germany’s planned reductions in future replacement rates — aim to stabilize finances but transfer more risk to individuals, challenging traditional social contracts.

The Advanced Multi-Pillar model: This includes the Netherlands, Canada, Norway and Australia, and represents a multi-tier hybrid system that deliberately diversifies across pillars (notably a strong universal basic pension plus quasi-mandatory occupational funding), often associated with balanced performance and long-term resilience. In Norway’s case, a substantial sovereign wealth fund helps buffer demographic and market shocks. However, these systems require high governance capacity and careful coordination. The need to better serve self-employed workers who fall outside standard occupational plans is another challenge.

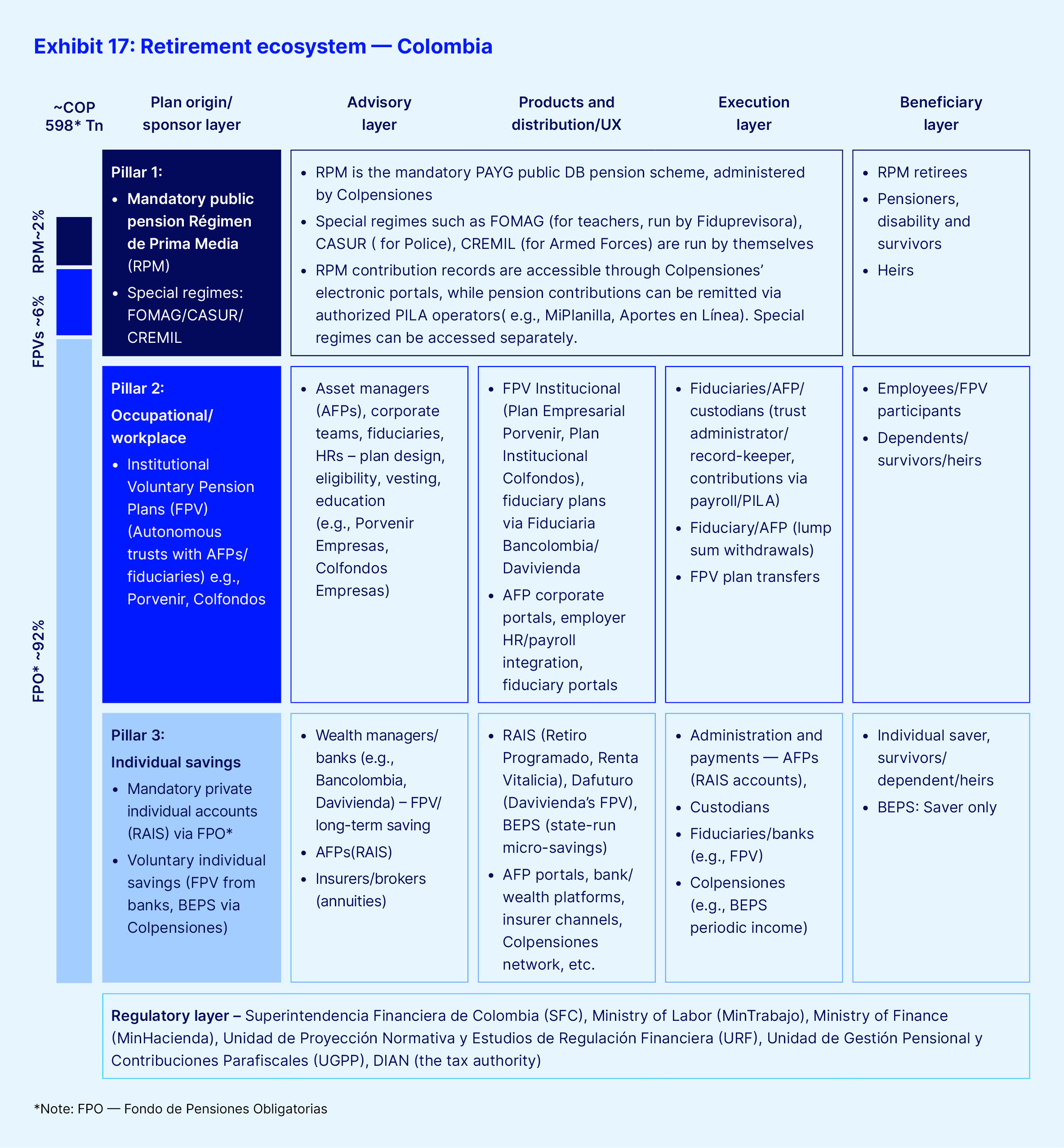

The Latin American model: This includes Chile, Mexico and Colombia, and shifts the center of gravity to mandatory funded DC (Pillar 2) with a safety net (Pillar 0), improving long-run public balance sheets yet making outcomes highly sensitive to contribution density, fees and drawdown design. Chile and Mexico fall under this category. The primary strength of this archetype is fiscal sustainability as the public PAYG liabilities are capped or eliminated. Over time, however, widespread informality and insufficient contribution rates have produced inadequate benefits, sparking public dissatisfaction and prompting a rebalancing toward multi-pillar designs that reinforce social assistance and integrate solidarity-based elements to improve equity. Colombia can also fall under this category with a distinct characteristic where workers can choose either a traditional PAYG public DB plan or a funded individual account, achieving risk diversification at the system level yet exhibiting similar weakness as the second archetype, to a certain extent.

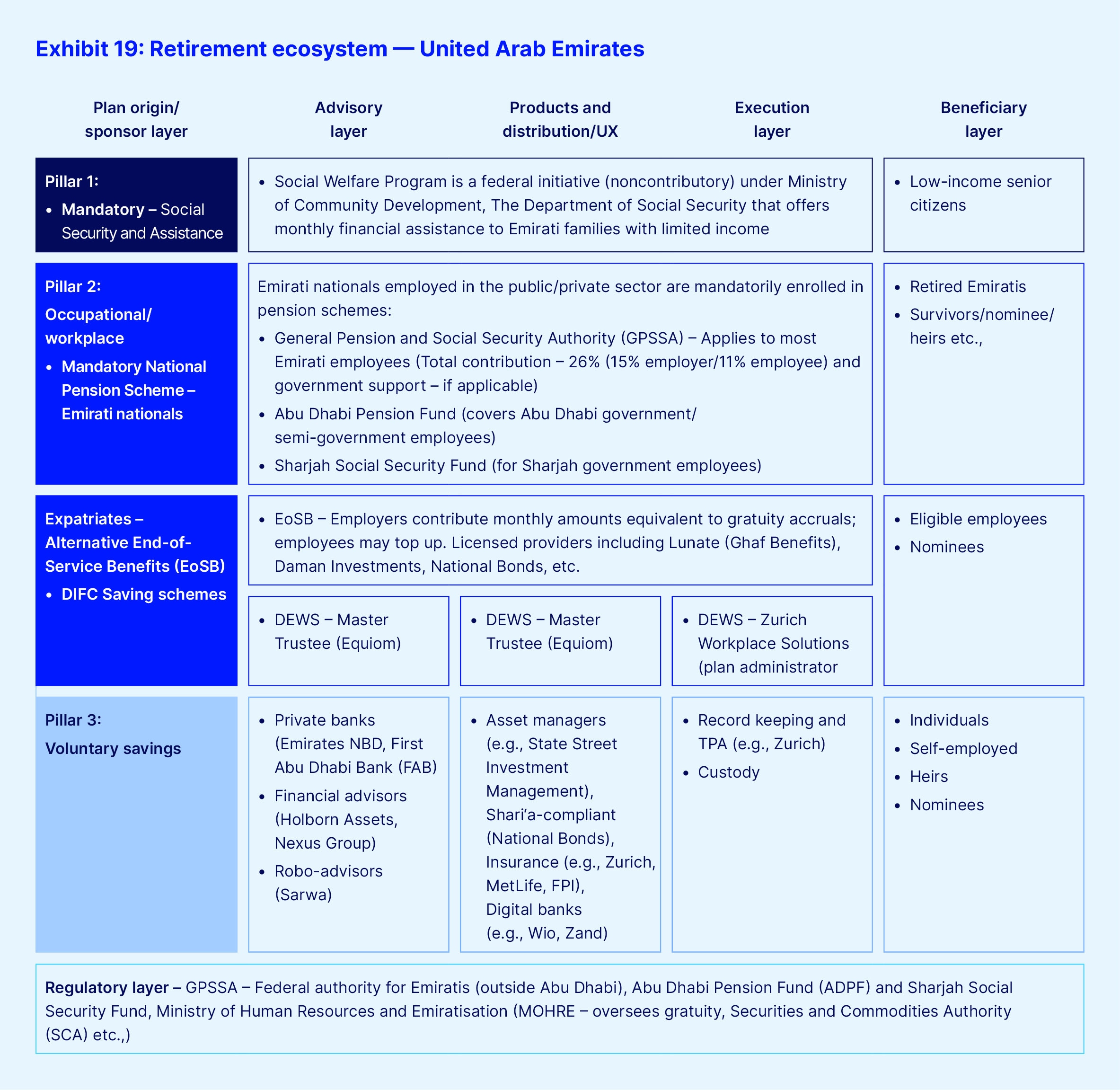

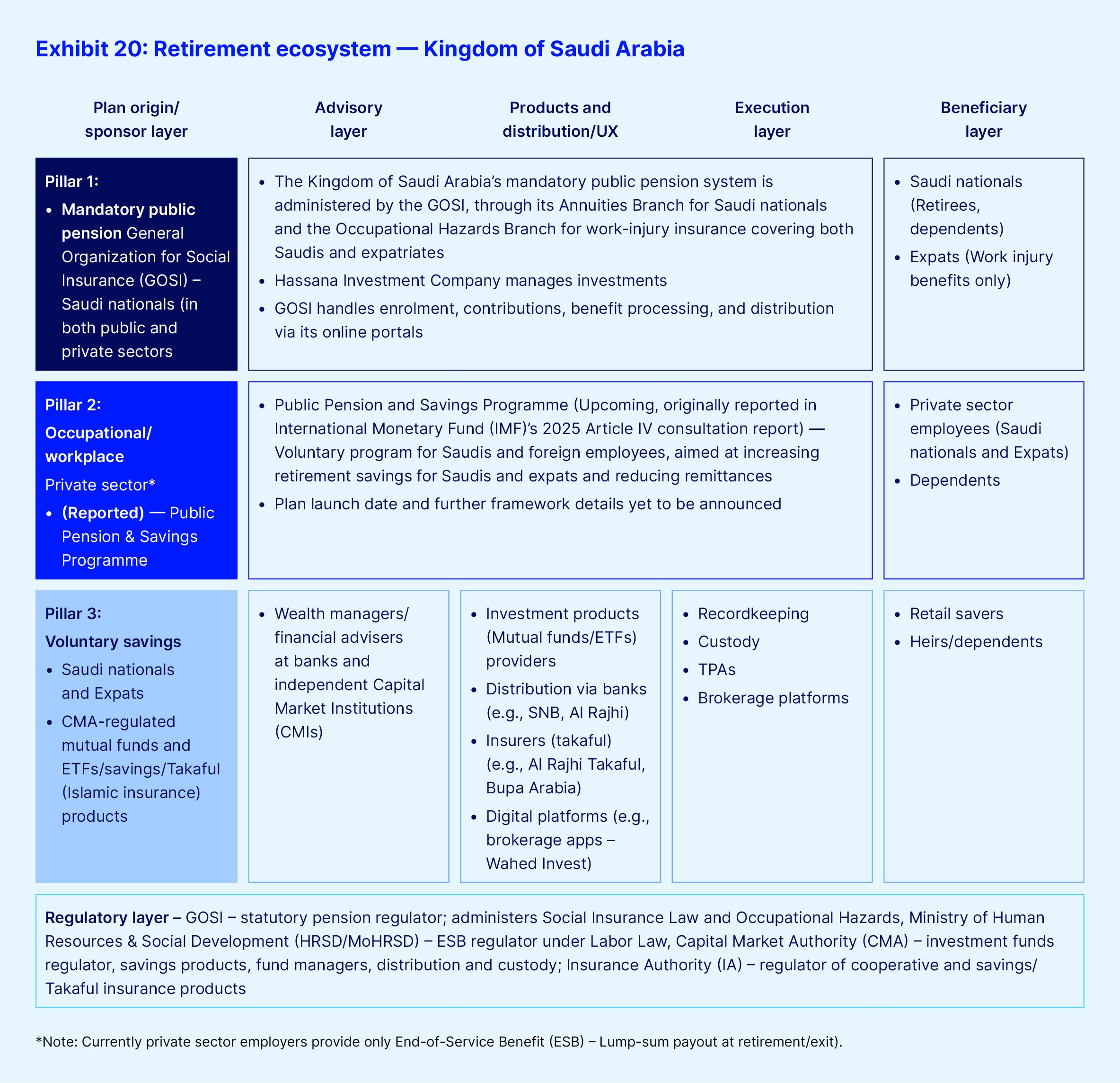

The Gulf model: This includes the Kingdom of Saudi Arabia (KSA) and the United Arab Emirates (UAE) and represents a resource-backed DB system that combines generous public pensions for citizens and end-of-service benefits for expatriates. While adequacy and coverage is strong for those who are covered, coverage is a serious issue for the system as expatriate workers make up the majority of the total labor force. Heavy reliance on Pillar 1 also puts a burden on state fiscal capacity. As a result, these systems are introducing reforms — higher retirement ages, pension fund mergers and new funded savings schemes for expatriates — to strengthen sustainability and modernize their retirement architecture.

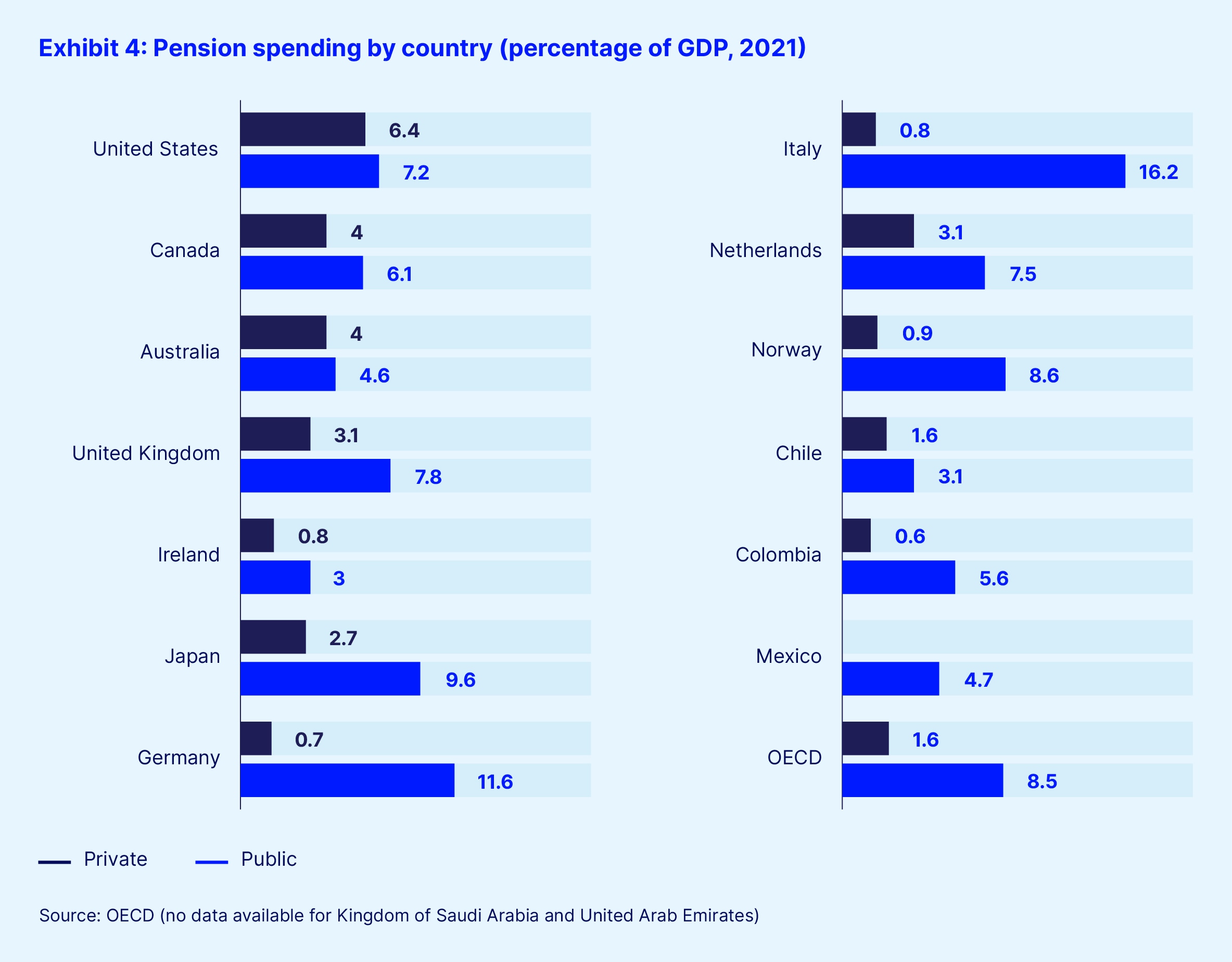

Some of the distinctions between these five retirement models can be observed in Exhibit 4.

Collectively, these models reveal a global trend toward balancing fiscal sustainability with adequacy, navigating demographic headwinds and adapting coverage mechanisms to increasingly diverse labor markets.

Opportunities for financial services

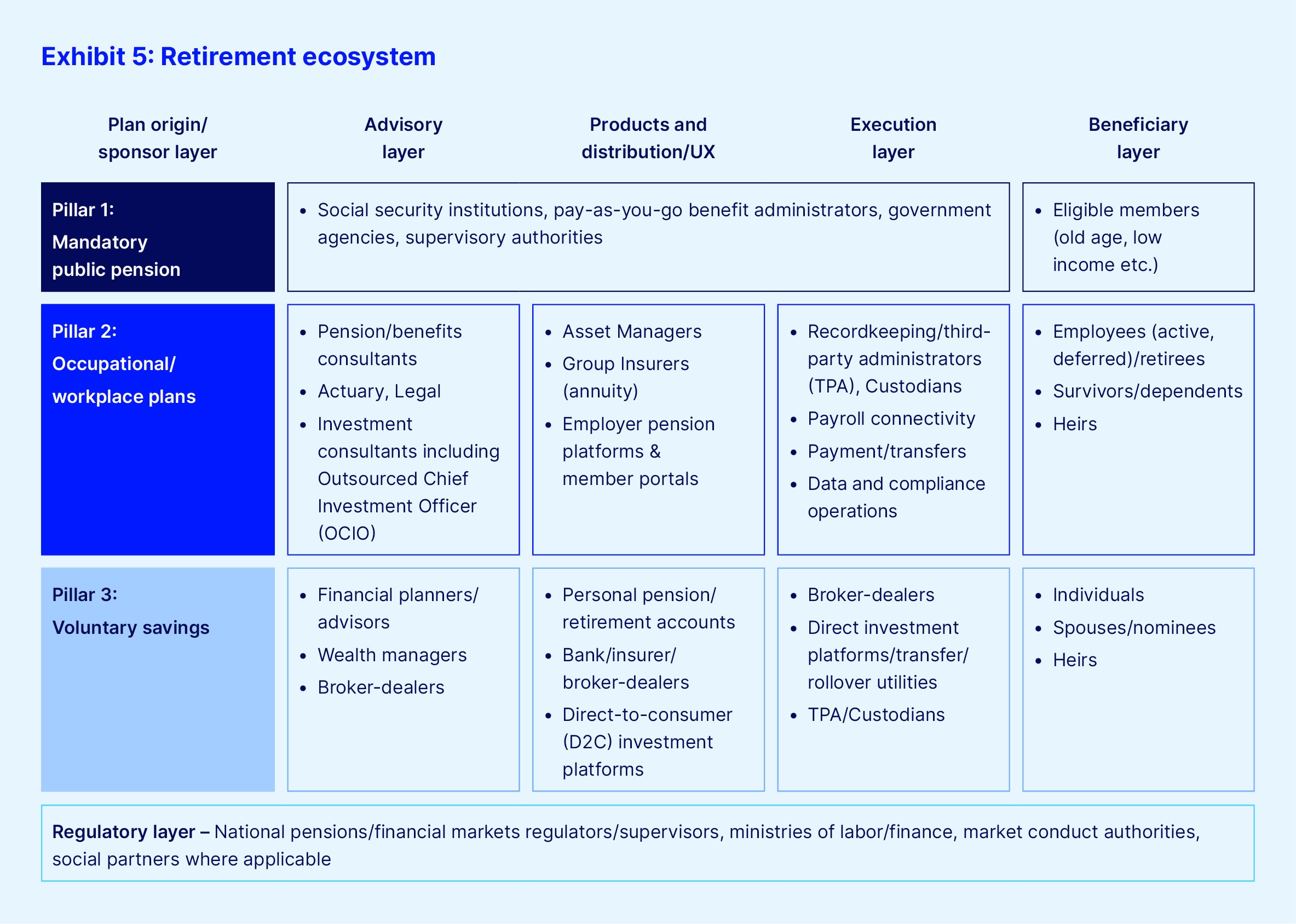

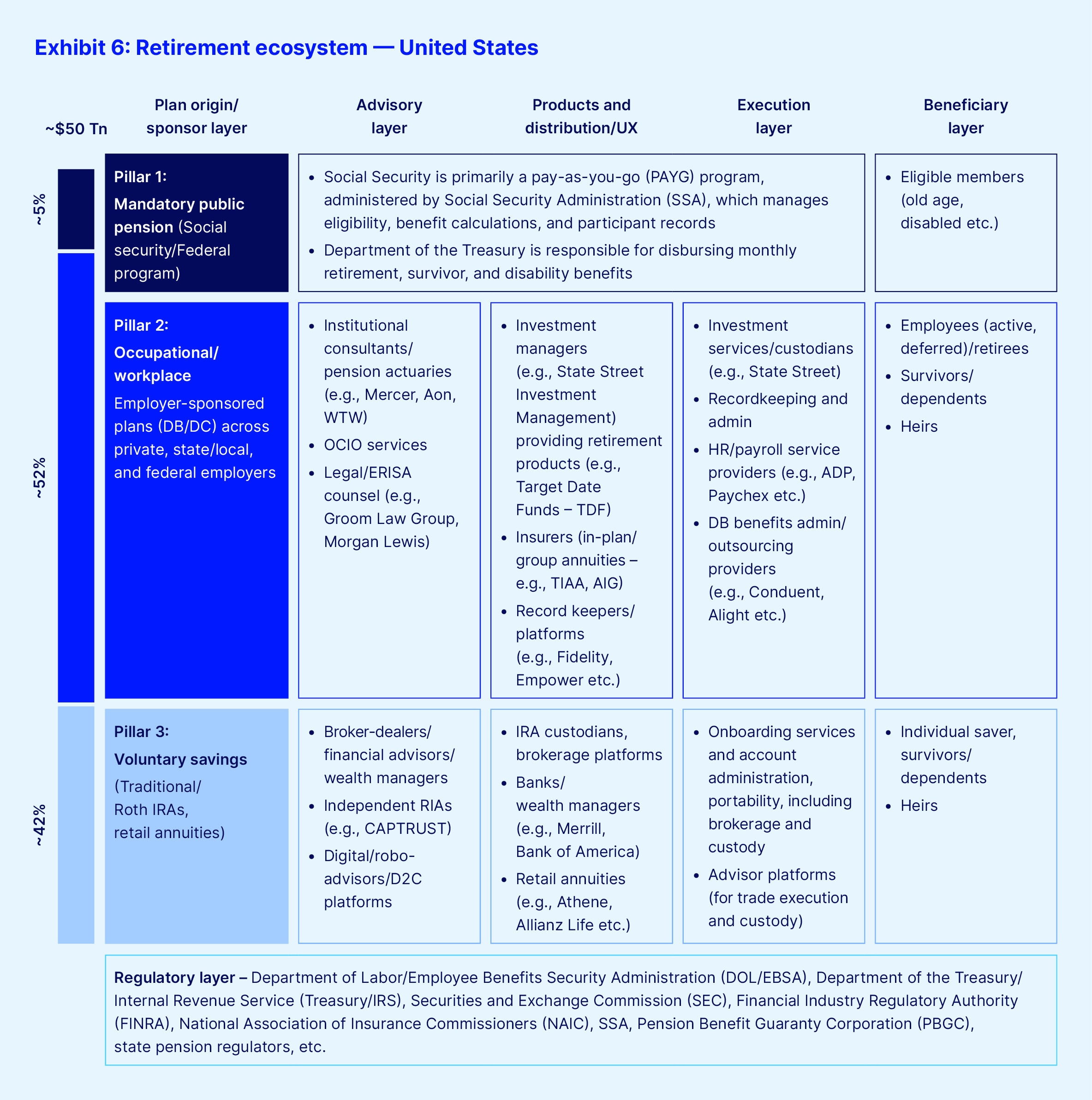

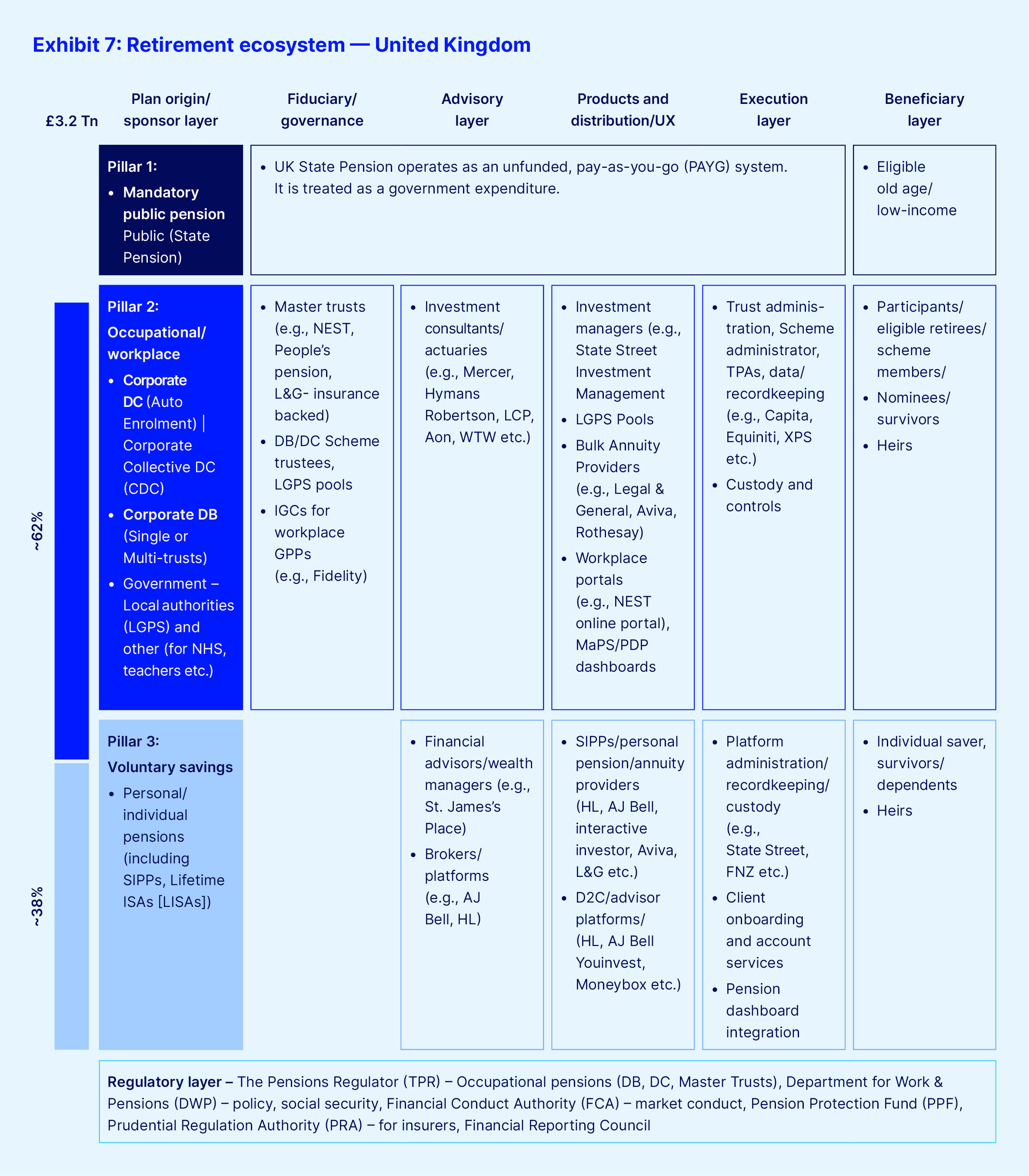

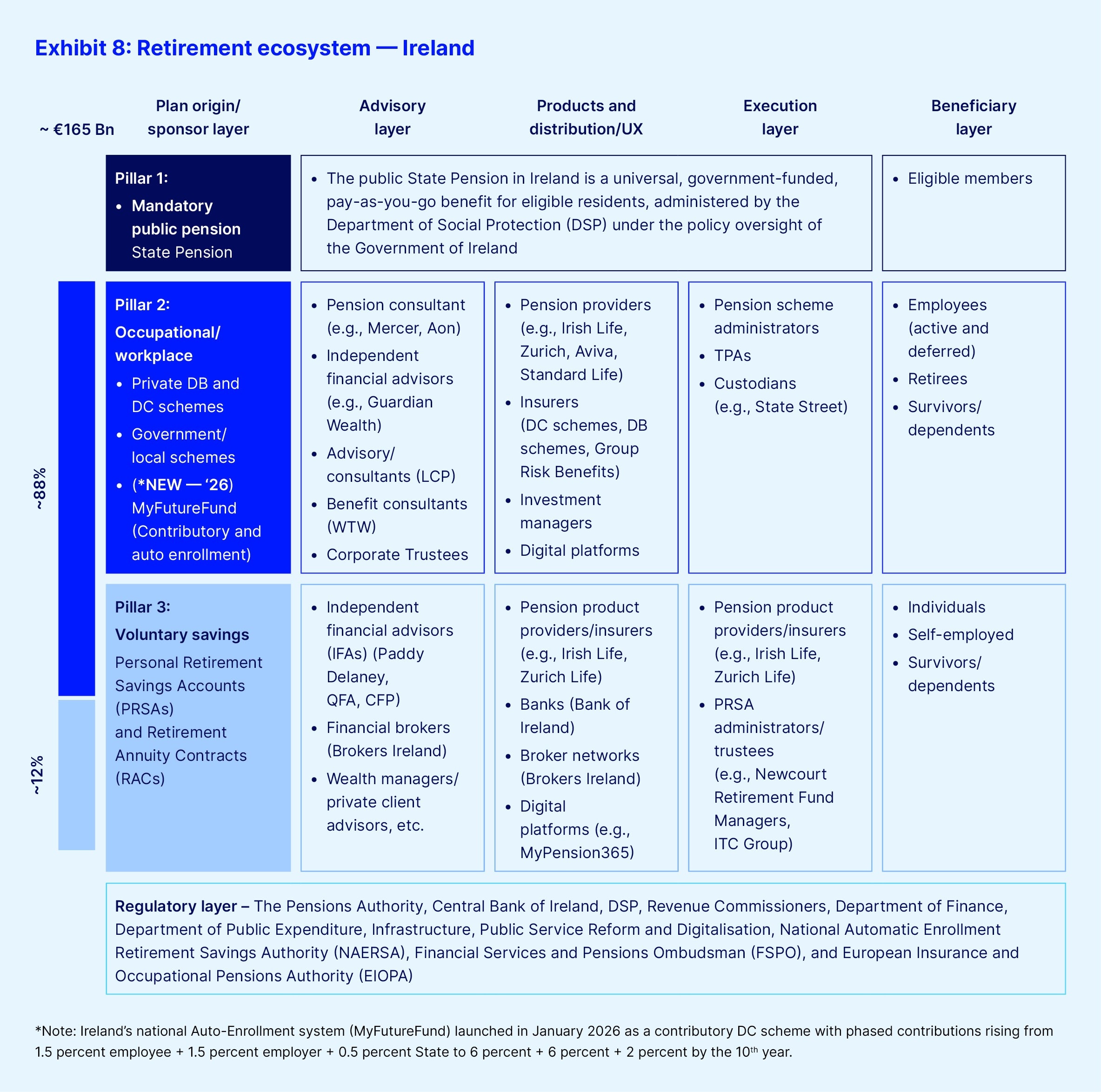

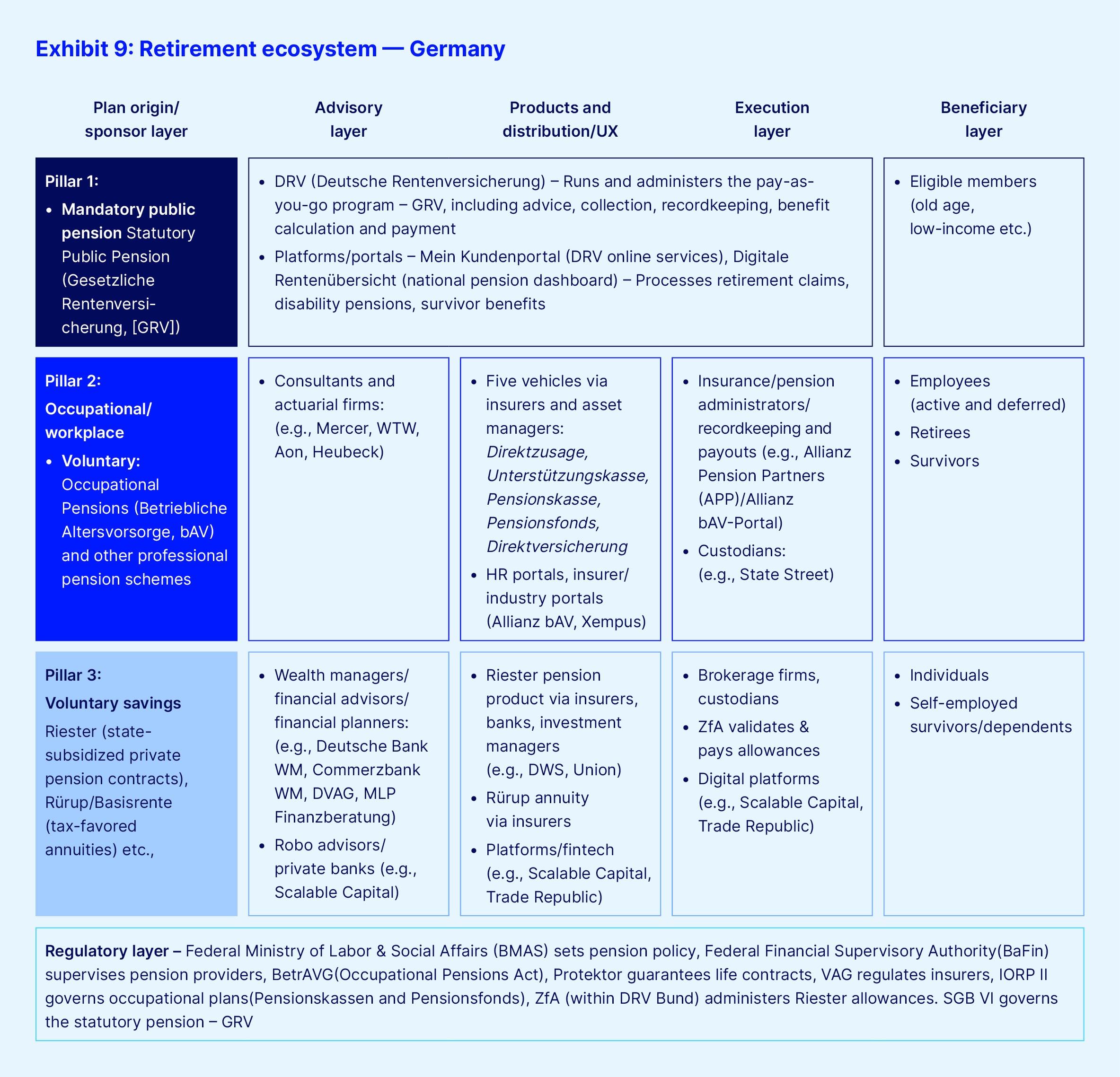

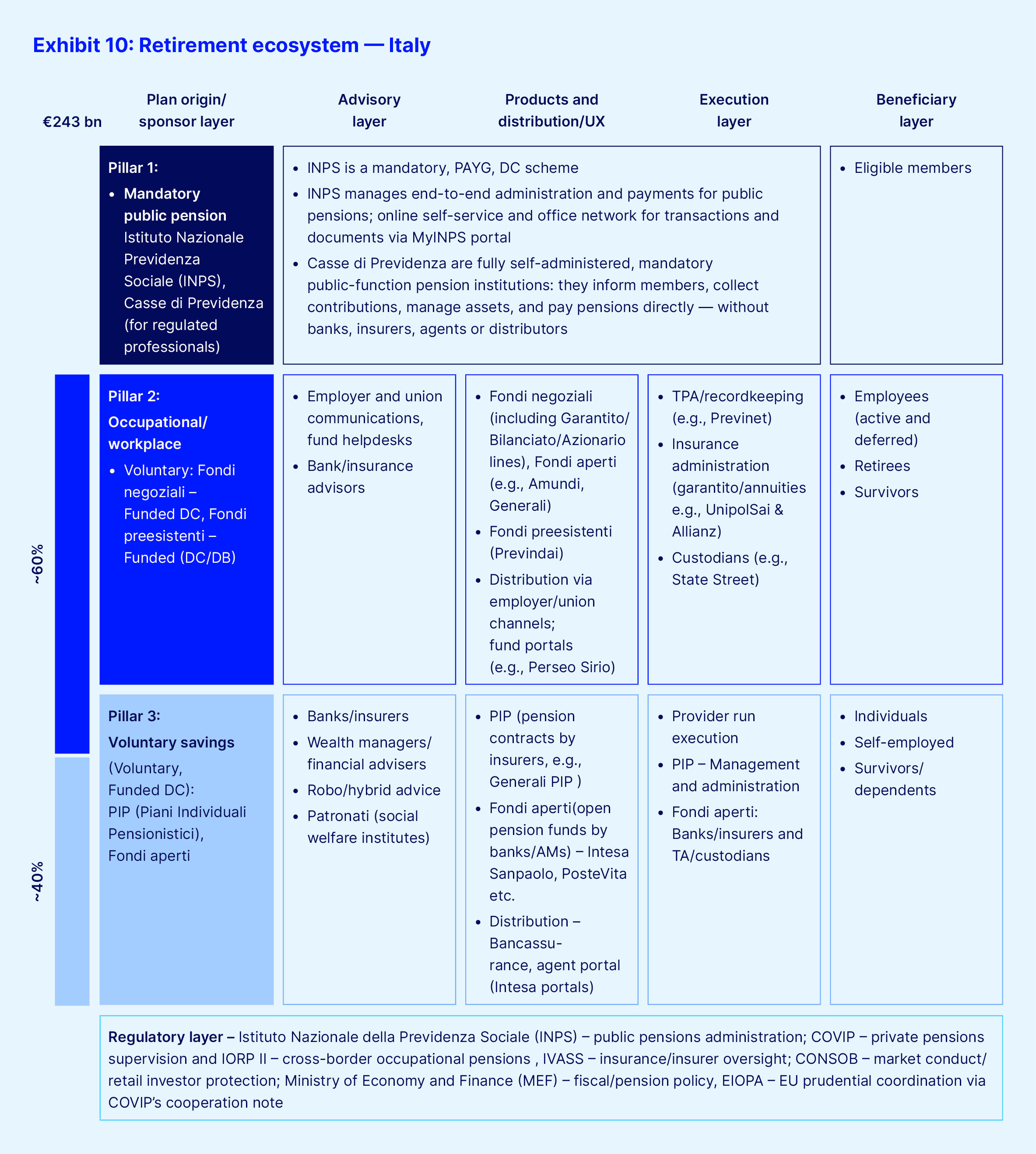

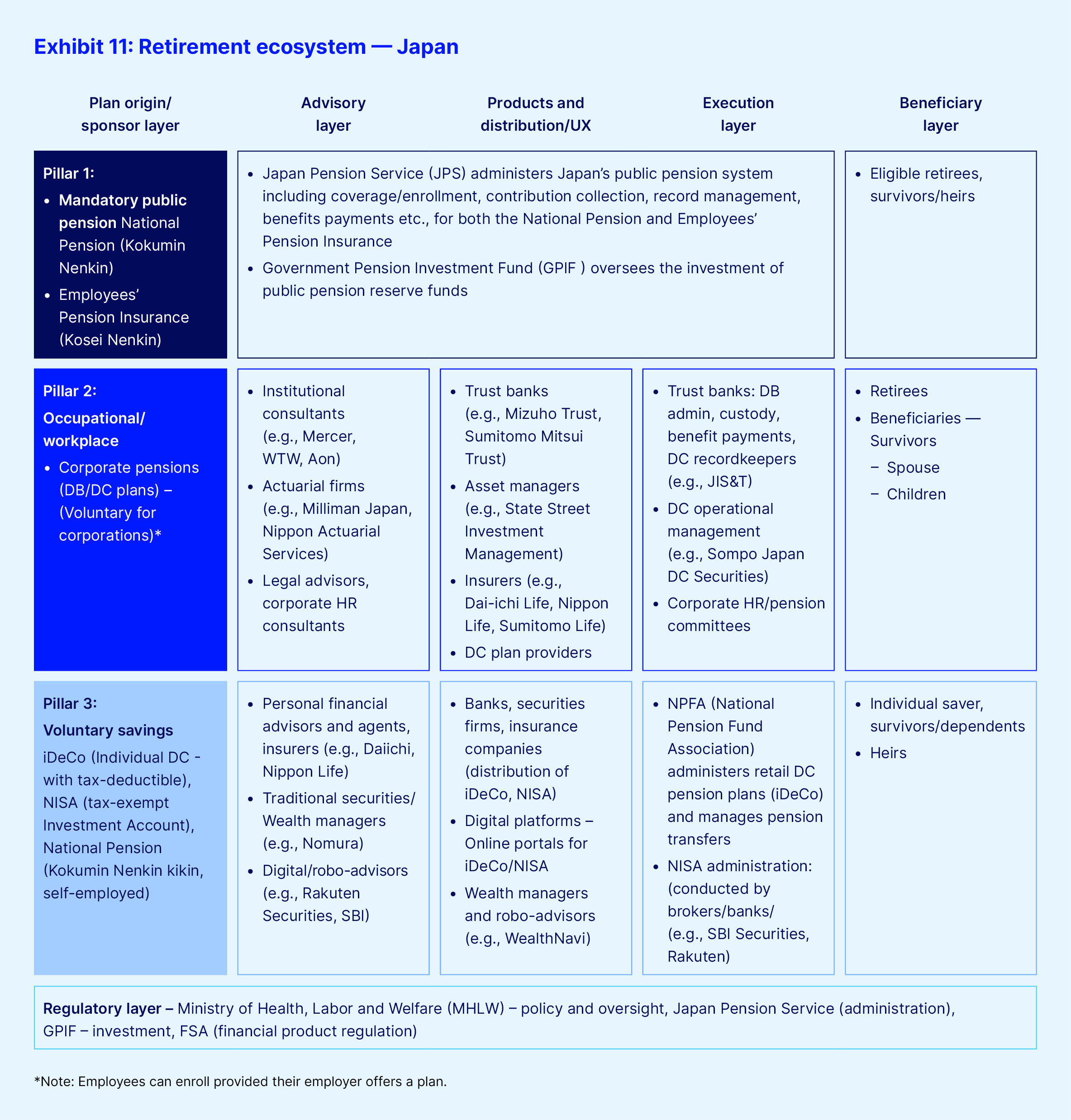

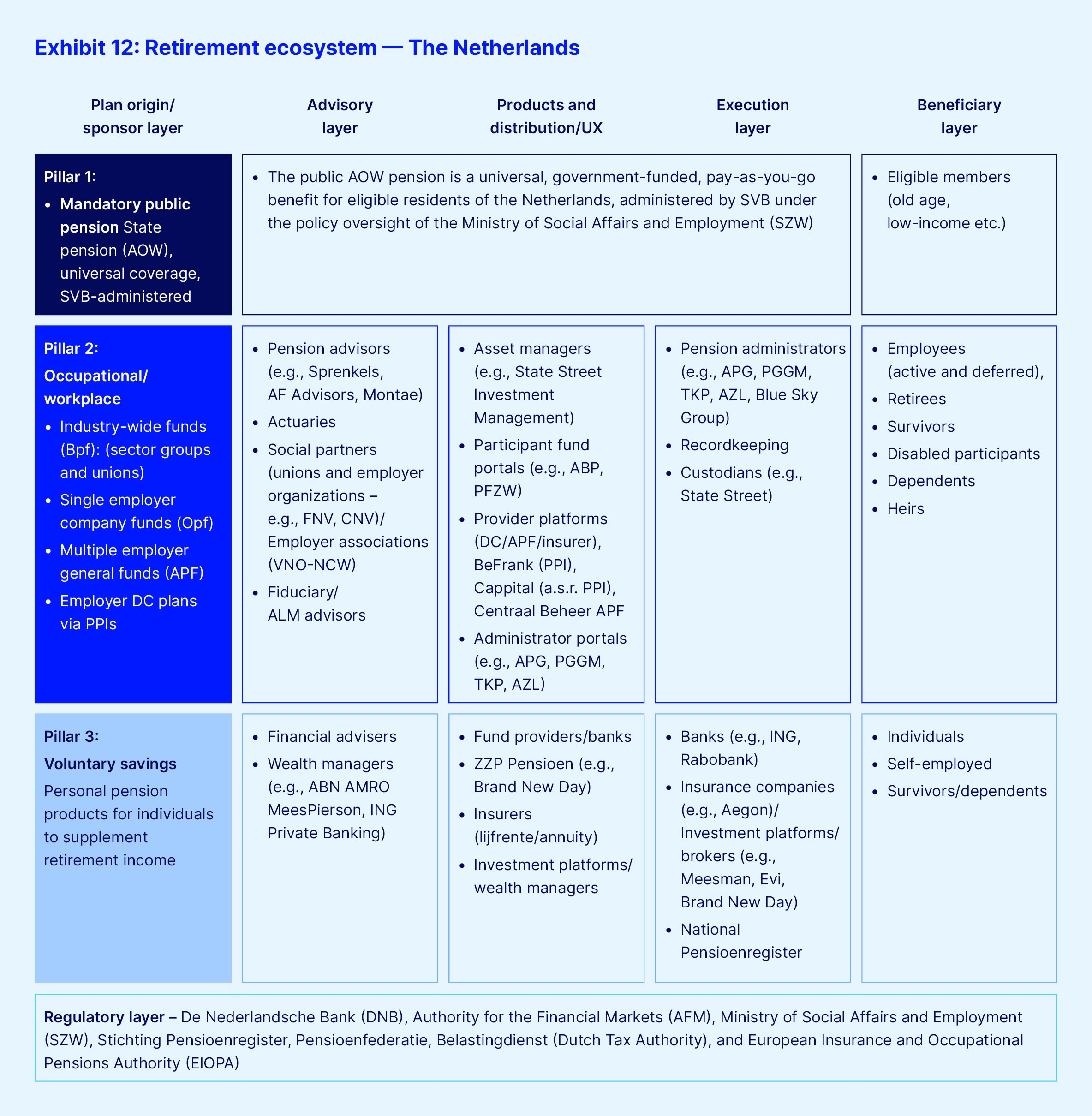

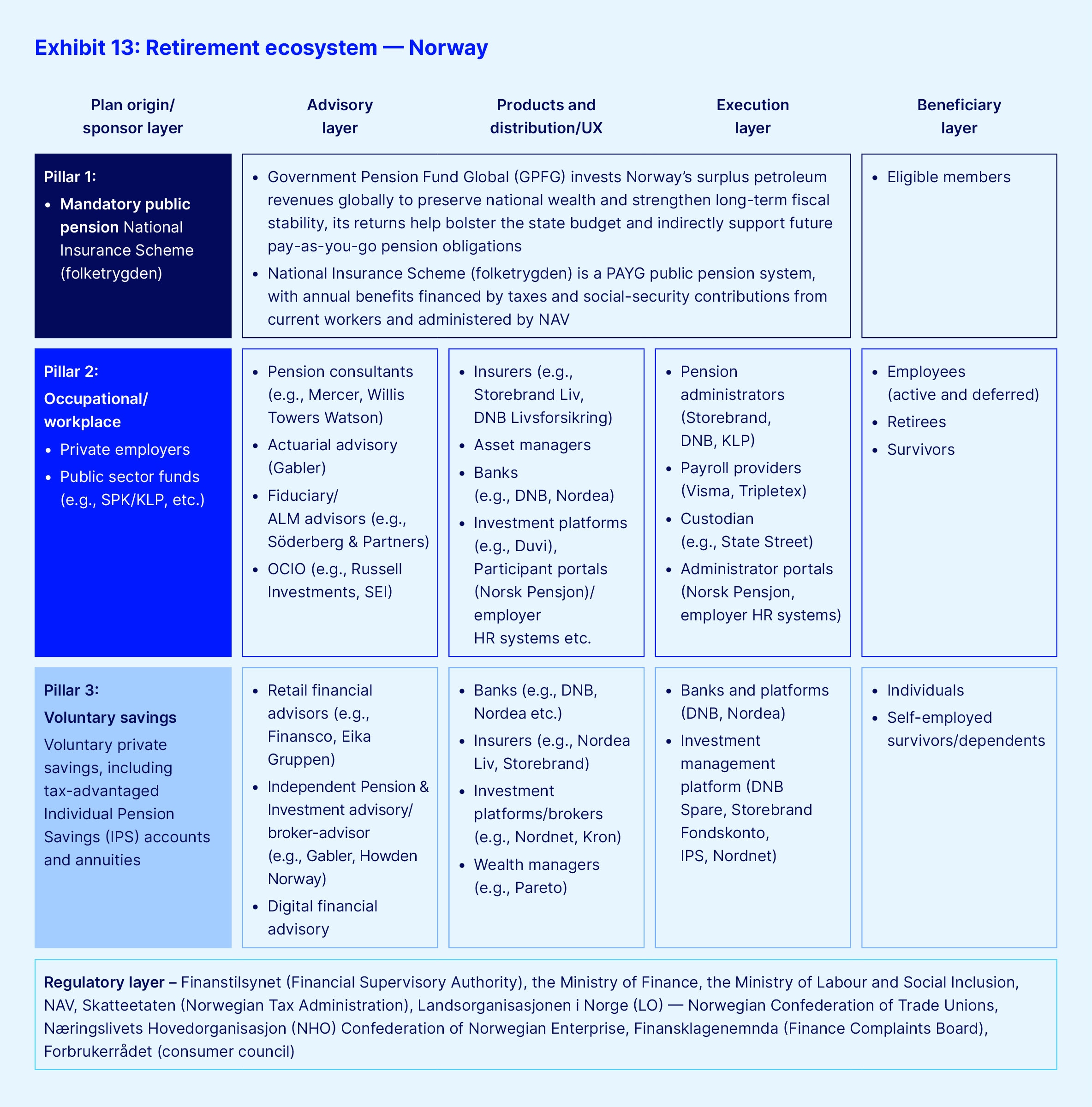

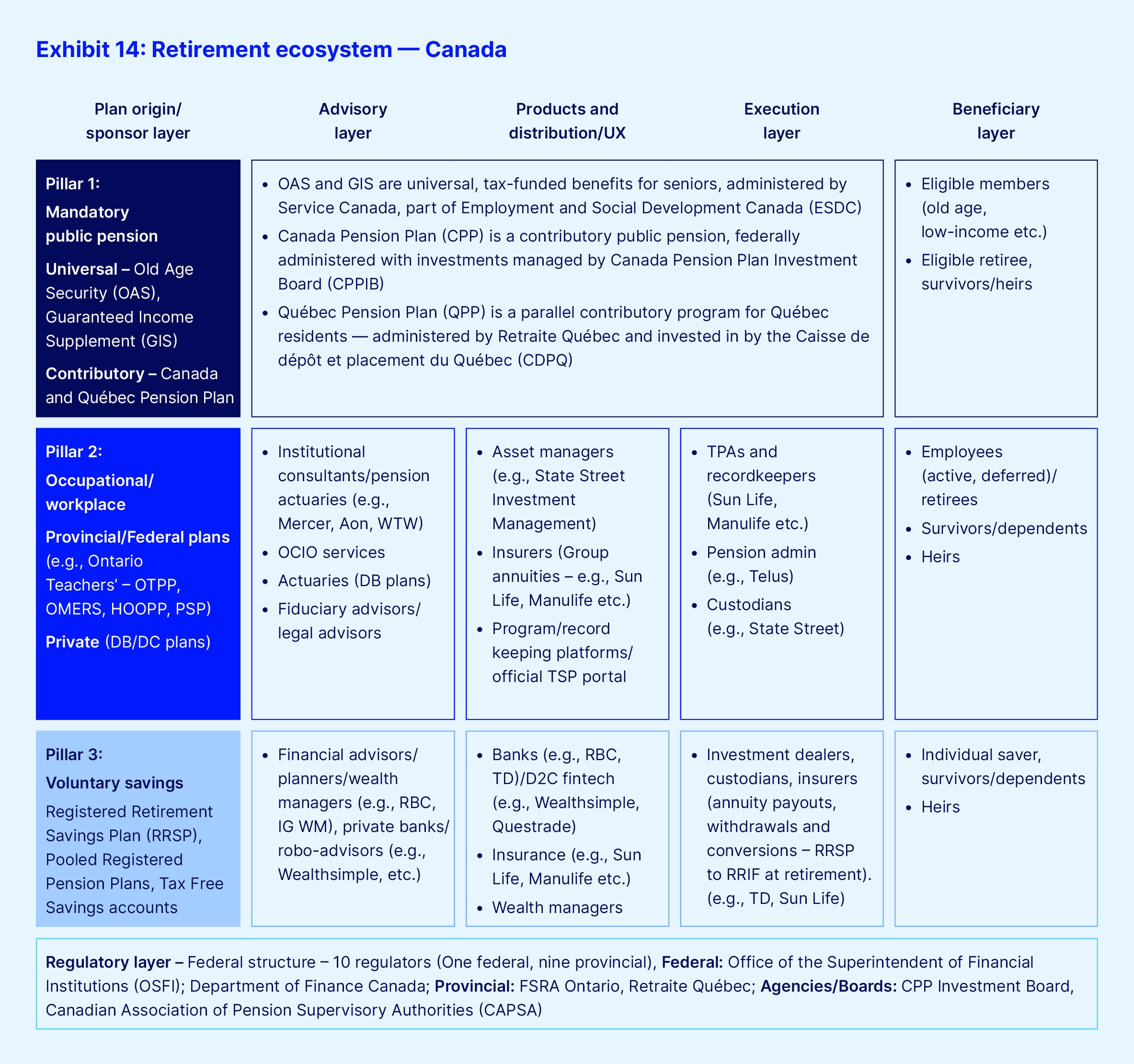

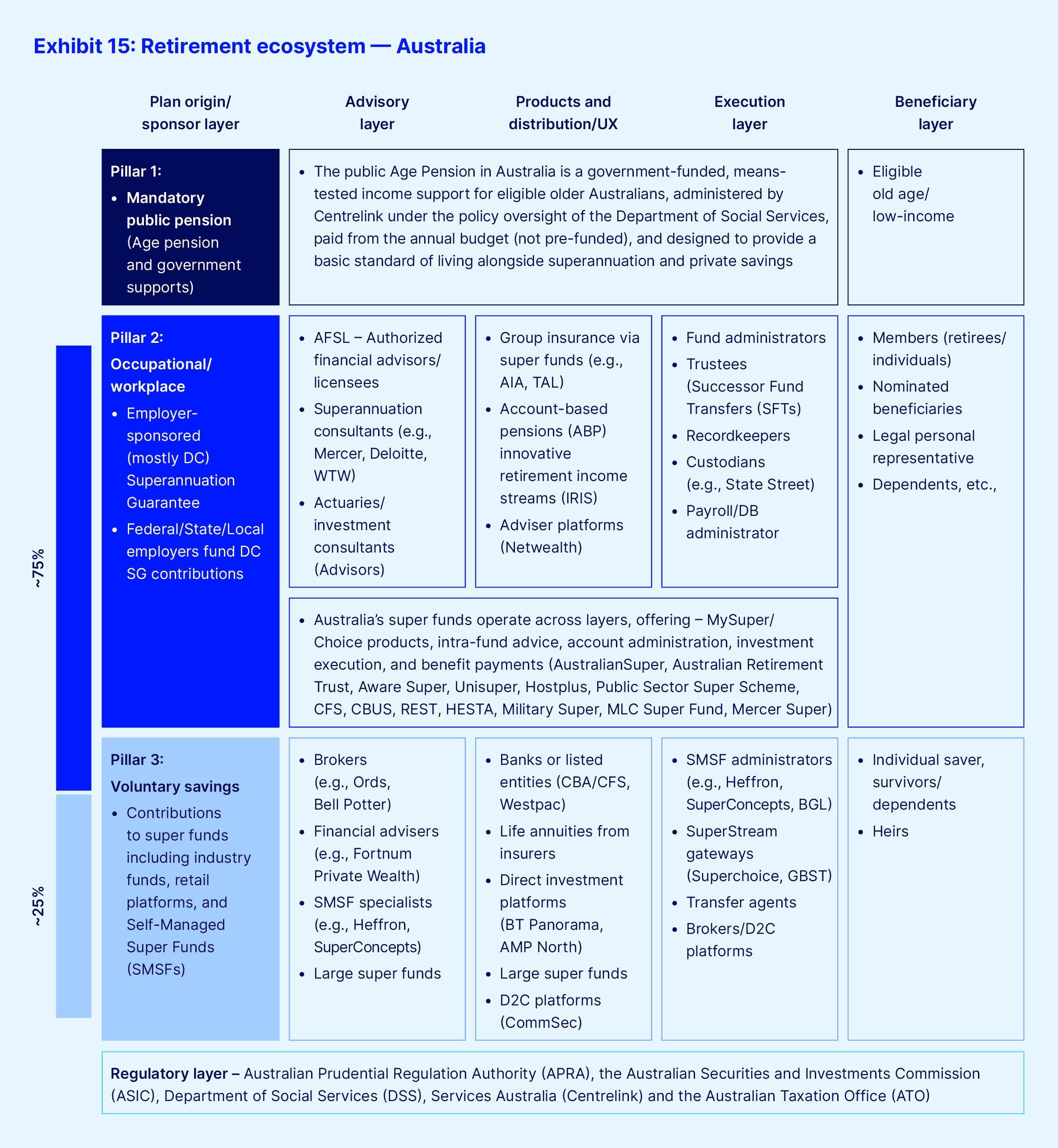

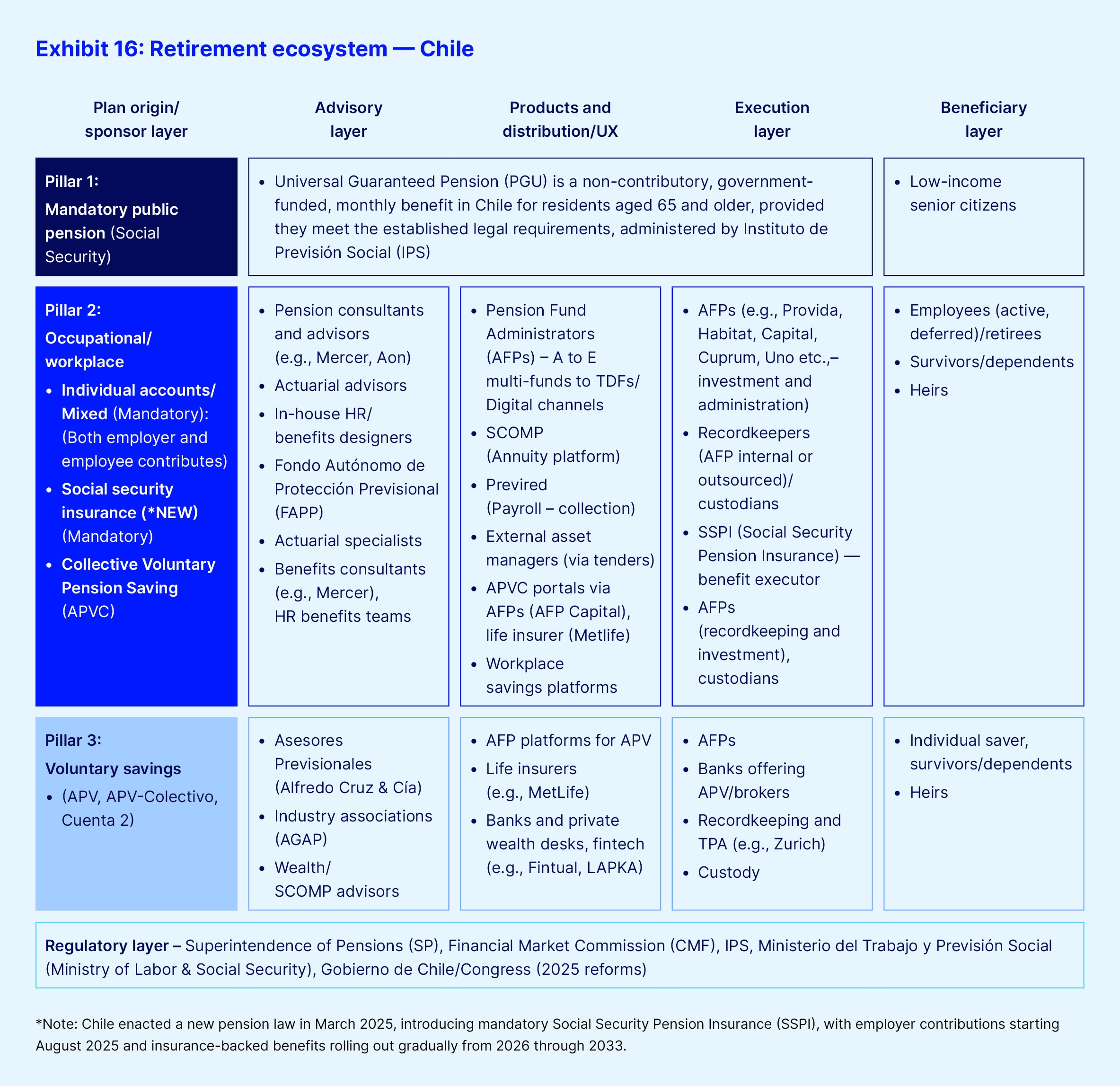

Our analysis connects macro and micro views — pinpointing who is affected by shifts in the global retirement landscape and where opportunities exist for financial services. We developed a retirement ecosystem view of each country (see Exhibit 5), mapping the end-to-end network of actors that together shape how retirement systems are designed, funded, administered and experienced by members.

We define a retirement ecosystem as the interconnected set of sponsors, advisors, product providers, custodians, administrators, regulators and participants that collectively create, fund, invest, administer and deliver retirement benefits. Across countries, the familiar pillar architecture is visible within this ecosystem: a public pillar (state pension or mandatory schemes); an occupational pillar (employer or sector plans, DB and/or DC); and an individual/retail pillar (personal savings vehicles and annuities). Accordingly, our ecosystem lens excludes Pillar 0 and Pillar 4, focusing on areas where financial services have the greatest ability to influence outcomes.

This allows the ecosystem framework to remain practical, decision-relevant and oriented toward areas where financial services capabilities can meaningfully drive change.

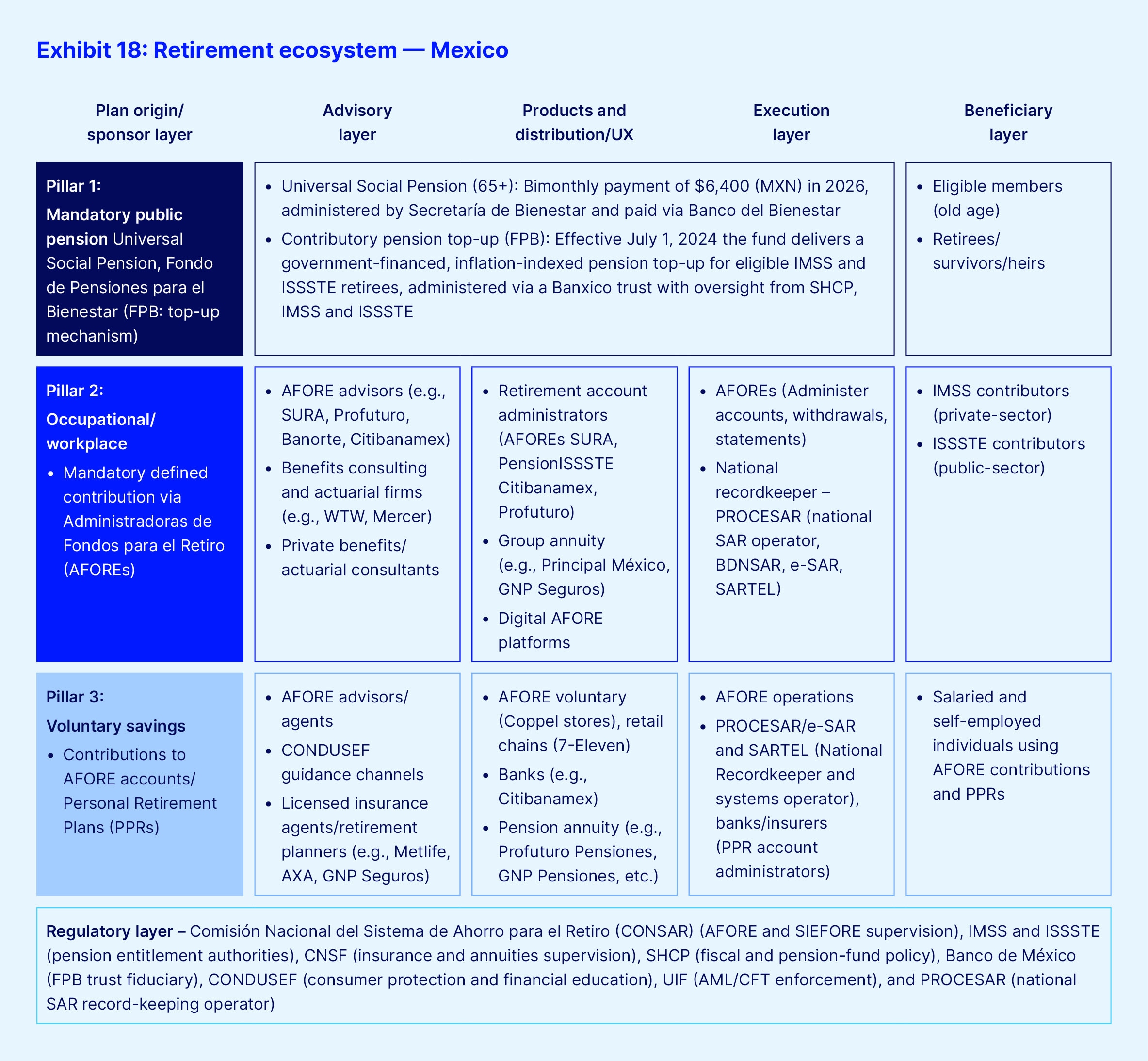

All retirement ecosystems are moving, to varying degrees, toward portable DC accumulation and more flexible decumulation, even where legacy DB remains material (e.g., UK and Canada). Day-to-day operations depend on specialized administrators and custodians, and each country has robust supervisory regimes. Beneficiaries ultimately include employees, the self-employed, retirees and their families, with outcomes shaped by decisions made across the retirement ecosystem. (See Country System Profiles for individual retirement ecosystems. These individual ecosystems are not meant to be exhaustive but illustrative, and they include examples of key stakeholders in different categories.)

Our macro analysis shows that while every country faces retirement system challenges, those pressures also create opportunities for financial services firms to provide solutions.

These opportunities can be understood as “value pools” — concentrated pockets of economic profit and growth that emerge where providers solve the most pressing member and sponsor problems at scale using repeatable, capital-efficient models.

Across advanced and emerging economies, all retirement systems are coalescing around six repeatable value pools.3 These include:

1. Decumulation and retirement income: The next growth S-curve

Decumulation has moved to the center of the retirement agenda. As cohorts relying on DC savings as their primary source of income enter retirement, the question is no longer how much they have saved, but how reliably those balances can be translated into income for life. Retirement ecosystems that are pulling ahead are doing so by standardizing a simple default pathway, combining guided drawdown with risk pooling and, where appropriate, partial annuitization or deferred income components. The aim is to give members predictable income, flexibility when circumstances change, and clear guardrails that reduce the risk of poor sequencing or longevity outcomes.

In the UK, roughly £1.2 trillion in DC assets now support rapidly rising withdrawals. Approximately 962,000 retirement accounts were accessed in 2024-2025, with about £70.9 billion withdrawn, and leading master trusts have begun launching decumulation defaults that blend drawdown with risk pooling. The Netherlands is finalizing a system-wide transition to DC by January 1, 2028, while a 10 percent lump sum cash withdrawal option from July 2026 has placed payout design at the heart of cohort communications. In Japan, super-aged demographics are producing explicit demand for guaranteed income, with strong interest in annuities that incorporate health-contingent features and a clear preference for lifetime income. Australia is approaching a tipping point, with annual contributions near A$160 billion and withdrawals around A$120 billion; projections indicate decumulation will overtake accumulation in the early 2060s. By contrast, Italy still tilts heavily to lump sum cash withdrawals — about €5.2 billion in 2024 versus roughly €361 million in annuities — highlighting the size of the opportunity for better income defaults. The US faces a 2026-2027 retirement surge while roughly half of retirees report lacking a withdrawal plan, underscoring the need for protective defaults that are easy to adopt.

There are implications for the financial services industry. Providers should build “operate-to-outcome” decumulation models that scale across cohorts, integrate modular risk pooling, and industrialize hybrid advice at retirement. Reporting should evolve from account balances to income sustainability — probability of success, longevity coverage and inflation resilience — so members and fiduciaries can judge outcomes through the right lens.

2. Digital engagement and hybrid advice: Dashboards as distribution

Digital engagement is becoming the distribution backbone of retirement. National dashboards and fund apps now consolidate lifetime data and surface the “next best action,” whether it is consolidating retirement accounts, adjusting contributions or selecting an income pathway. When hybrid advice — a well-designed blend of digital guidance and human expertise — is embedded into these journeys, participation can rise, investment quality can improve and at-retirement conversions can accelerate.

The operating model is visible across markets. In Germany, the Digitale Rentenübersicht is live, aggregating roughly 137 million records from more than 700 providers and enabling dashboard-integrated guidance across pillars. Norway already demonstrates the next step: Norsk Pensjon, the social security agency NAV and major banks use centralized data to run mobile calculators and hybrid advisory journeys for approximately 2.21 million EPK accounts (about NOK641 billion), enabling personalization and friction-light switching.

The UK is preparing pensions dashboards that should enable one-click consolidation at the same time that only about nine percent of adults receive full advice, creating a clear case for scaled hybrid models. Australia shows strong bottom-up demand, with Gen Z app usage roughly sevenfold higher than five years ago and more than 600,000 younger members engaging via mobile. Japan adds a technology-first policy backdrop through Society 5.0 (a long-term national policy framework), while Saudi Arabia is building digital-first retirement experiences on near-ubiquitous smartphone penetration. Ireland’s 2026 auto-enrollment launch will benefit from the same approach: digital onboarding, consented data-sharing and literacy nudges.

Financial services firms could consider building a modular, interoperable engagement layer that allows dashboards, data sources and advice tools to connect seamlessly, operationalize triage-based hybrid advice at scale, institutionalize behavioral design and harden cyber-resilience. The goal is to convert raw data into compliant, personalized actions that members can complete in minutes, not weeks.

3. Coverage expansion and portability: Unlocking new contributors and assets

Coverage expansion and portability reforms are bringing part-time, gig and expatriate workers into funded arrangements with savings that follow them across jobs and borders. Retirement systems are moving from fragmented, one-off benefits toward portable accounts that reduce leakage and lift adequacy, especially for groups historically excluded from second-pillar plans.

Several reforms are reshaping the addressable market. Ireland launched MyFutureFund auto-enrollment in January 2026, with rising assets and employer participation reinforced by rapid master trust consolidation. The UAE has begun replacing end-of-service gratuities with funded workplace pensions, evidenced by the Dubai Employee Workplace Savings (DEWS) scheme surpassing US$1 billion and the rollout of a Federal Alternative End-of-Service Benefit (EOSB) framework, giving employees portable accounts rather than one-time cash. Saudi Arabia’s forthcoming Public Pension & Savings Programme (2025/26) will bring approximately 10 million expatriates into formal savings while raising contributions and aligning the retirement age to 65. In the Netherlands, DC conversion improves portability of accrued rights with a parallel focus on engaging the self-employed. Japan is extending eligibility to part-time and non-regular workers, and broadening the use of Individual-type Defined Contribution Pension (iDeCo) and Nippon Individual Savings Account (NISA), and Australia’s “stapling” reform assigns each worker a single superannuation account that follows them between jobs, materially lowering duplication and leakage.

A major implication for financial services is to treat coverage expansion as a distribution pipeline, automating employer onboarding, simplifying eligibility checks, and defaulting members into sensible portfolios from day one. Firms should also offer portable wrappers that work across employers and, where policy allows, across borders; embed literacy and micro-nudges at enrollment to establish contribution adequacy early, and design inclusive products that accommodate irregular earnings and smaller balances without punitive fees.

4. Institutional risk transfer and endgame: Scaling fast

As DB funding improves, sponsors are prioritizing certainty through pension risk transfer and endgame strategies. Scale advantages increasingly accrue to institutions that combine capital, underwriting, administration and asset origination into coherent “endgame factories,” giving trustees high-confidence execution while protecting members.

The trend is most visible in the UK, where aggregate DB funding near 130 percent is powering a sustained surge in bulk purchase annuity volumes, on the order of £45-50 billion per year, and expanding to sub-£100 million schemes as insurer capacity grows. Canada shows a similar pattern, with group-annuity pension risk transfer setting a record near-C$11 billion in 2024, as sponsors offload longevity and investment risk into specialist balance sheets.

Financial services firms should build, or partner to assemble, a full endgame stack: balance-sheet capacity and reinsurance, industrial-grade administration, member communications and liability-aware asset origination. Standardizing transition playbooks for data cleansing, benefit security, and stakeholder messaging is another important consideration, as is strengthening longevity risk management through hedging and reinsurance, and aligning asset portfolios (including private credit and real assets) to liability cash flows and inflation dynamics.

5. Scale capital to private markets and sustainability: The fee-resilient growth engine

Large retirement systems are rotating toward private markets to secure durable, inflation-linked returns and diversify away from public market beta. At the same time, sustainability considerations are increasingly shaping how that capital is governed, allocated and evaluated particularly in large, pooled systems where long-term stewardship, transparency and member outcomes are central to mandate design. Success depends on rigorous governance, liquidity management and transparent reporting that meets regulatory expectations.

Policy and practice are converging. In the UK, the Mansion House initiatives are nudging DC defaults toward 5-10 percent allocations to private markets by 2030, supported by vehicles such as the Long-Term Asset Fund. The Netherlands provides a clear example of sustainability at scale: PFZW has reallocated roughly €29 billion toward active sustainability-aligned strategies, concentrated its listed holdings and materially reduced portfolio carbon intensity. In Canada, the “Maple Eight” public funds manage more than C$2.4 trillion with significant private asset allocations, and are diffusing their model to mid-tier plans through partnerships and co-investments. Saudi Arabia, via Hassana (the investment arm of the General Organization for Social Insurance or GOSI), is diversifying a portfolio of about SAR1.2 trillion into global infrastructure, private equity and climate solutions, signaling growing demand for institutional-grade access platforms. Australia’s mega-funds are deepening private asset sleeves with embedded environmental, social and governance (ESG) processes and member-outcome reporting.

Here, the implications for financial services firms are profound. Considerations include: 1) Standing up DC-appropriate private market access using the right wrappers (for example, LTAFs or collective investment trusts) with pacing plans, liquidity sleeves and robust valuation governance. 2) Linking sustainability efforts to member outcomes with clear metrics — inflation resilience, net-zero alignment and carbon intensity — that are intelligible to non-specialists. 3) Building co-investment and origination capacity through partnerships with leading funds, and codify risk controls (stress testing, side-pockets and redemption gates) that align with regulation and fairness to members.

6. A cross-cutting demand driver: Women’s wealth and younger cohorts

Across many retirement systems, rising women’s wealth and the digital engagement of younger cohorts are acting as powerful cross-cutting demand drivers that amplify each of the major value pools. These dynamics are particularly pronounced in the US, Australia, the Netherlands and Italy, and they carry direct implications for product design, advice models and member engagement strategies.

In the US, women are expected to control approximately US$34 trillion by 2030, representing nearly 38 percent of total investable assets. Over the longer term, women are projected to inherit roughly 70 percent of the US$124 trillion “Great Wealth Transfer” by 2048, materially reshaping demand across advice, protection and retirement income. This shift is accelerating the need for solutions that address longer life expectancy, caregiving interruptions and preferences for income certainty, while also placing greater emphasis on holistic financial planning and intergenerational wealth strategies.

A similar but even more concentrated dynamic is emerging in Australia, where women are expected to inherit an estimated A$3.2 trillion over the next decade, accounting for roughly 65 percent of total intergenerational transfers. At the same time, engagement from Gen Z and Millennial cohorts is rising sharply through superannuation mobile apps and digital platforms. Together, these forces heighten the importance of intuitive product design, mobile-first user experience and advice frameworks that reflect women’s longevity profiles and younger savers’ expectations for transparency, personalization and sustainability.

In the Netherlands, women’s economic independence is growing rapidly. This structural shift is reinforcing preferences for sustainable investing, life event-based planning and shared financial decision-making within households. These preferences are being actively embedded into the country’s new DC architecture, where communication, cohort-based outcomes and sustainability credentials play an increasingly prominent role in member engagement.

By contrast, Italy highlights the remaining upside where these dynamics have not yet been fully addressed. Participation in supplementary pension schemes remains skewed approximately 62 percent male, reflecting lower workforce participation, career breaks and lower engagement among women. As a result, targeted product design — encompassing simplified advice journeys, improved portability and female-focused engagement strategies — represents an immediate and tangible growth lever for providers seeking to broaden participation and improve retirement adequacy.

There are clear implications across countries. Women’s rising share of retirement wealth, combined with the digital expectations of younger cohorts, is not a niche trend but a structural force shaping demand across accumulation, decumulation, advice and investment design. Financial services firms that embed these considerations — through tailored income solutions, flexible contribution and withdrawal features, intuitive digital journeys, and credible sustainability offerings — will be better positioned to capture growth across multiple value pools simultaneously.

Country system profiles

Design implications for the next phase of retirement systems

Taken together, the forces reshaping retirement systems point to a consistent pattern: While national systems differ in structure, governance and funding, the pressures acting on them are increasingly shared. Demographic aging, fiscal constraints, labor market fragmentation, and rising expectations for security and adequacy are no longer testing individual features of system design, but the way systems allocate risk and responsibility overall. What increasingly differentiates systems is not the challenge itself, but how effectively architecture translates savings into durable outcomes.

Across countries, system architecture is proving decisive. Where risk is concentrated within a single pillar or borne disproportionately by individuals, pressures surface in the form of adequacy gaps, participation shortfalls or fiscal strain. When responsibility is more deliberately shared across public, occupational and individual mechanisms — and supported by effective governance and operational coordination — systems demonstrate greater resilience, adaptability and confidence among participants. The interaction across pillars, rather than the strength of any single component, is increasingly a primary determinant of outcomes.

This has important implications for decision-makers across the retirement ecosystem. Design choices — default structures, contribution pathways, risk-sharing mechanisms, decumulation options and governance frameworks — are now strategic levers. They shape not only financial stability, but participation, trust and the ability of systems to evolve alongside changing work patterns, longevity profiles and societal expectations.

Several considerations now emerge as central across markets:

- System coherence matters more than system type. No single model consistently outperforms across contexts. What distinguishes more resilient systems is alignment — between policy intent, product design, operational execution and participant experience.

- Risk is being re-priced, whether explicitly or implicitly. Longevity, inflation, market volatility and employment risk are shifting across pillars and stakeholders. Making these trade-offs explicit — and designing mechanisms to manage them — is increasingly critical.

- Decumulation is becoming the defining frontier. As balances grow and retirements lengthen, the conversion of savings into income is emerging as the most consequential design challenge across systems, regardless of funding model.

- Engagement and confidence are outcomes, not inputs. Participation, contribution adequacy and the effective use of retirement assets depend on systems that simplify decisions, align incentives and reinforce trust over time.

Looking ahead, retirement systems are moving toward greater emphasis on outcomes over accumulation, coordination over fragmentation, and stewardship alongside administration. For institutions, policymakers and market participants, both the opportunity and the responsibility lie in shaping architectures that not only withstand shared pressures, but actively channel them into more sustainable, inclusive and trusted retirement outcomes.

Decision implications for institutions and intermediaries

1. Architecture is now a strategic variable — not a background condition

Retirement outcomes are increasingly shaped by how systems are structured across pillars, not by performance or participation in isolation. For institutions and intermediaries operating within and across systems, understanding underlying architecture — funding flows, risk allocation, governance and coordination — is becoming as important as evaluating individual mandates, products or services.

2. Risk transfer is accelerating — often without redesign

Longevity, inflation, market and employment risks are shifting across governments, employers, institutions, intermediaries and individuals. In many systems, this transfer has occurred incrementally rather than by design. Organizations should assess where they sit in this risk chain — whether they are absorbing, intermediating, amplifying or mitigating risk — and whether that role is explicit, priced and sustainable.

3. Decumulation is emerging as the primary system constraint

As balances grow and retirement durations lengthen, the conversion of savings into income is becoming the defining challenge across systems. Institutions and intermediaries positioned to support income design, pooling, drawdown strategies and participant decision pathways will increasingly influence outcomes — regardless of whether systems are public, occupational or personal.

4. System fragmentation creates both risk and opportunity

Breakdowns across pillars — in governance, data, accountability and participant experience — increasingly drive inefficiency and uneven outcomes. Intermediaries often sit at these seams. Those with the capability to coordinate with stakeholders, bridge data and execution gaps, or simplify complexity are well positioned to add value at the system level. Operationally, partnering with leading recordkeepers, custodians and administrators to deliver unified portals, straight-through transfers and resilient cybersecurity strengthens trust and lowers cost.

5. Confidence is shaped by system design, not participant sophistication

Engagement, contribution adequacy and effective use of retirement assets depend less on education than on structures that simplify decisions and align incentives. Institutions and intermediaries that support design-led solutions — defaults, automation and guided pathways — can materially influence confidence and long-term outcomes while scale alliances can accelerate innovation.

6. The next phase of value creation is shared stewardship

Value is shifting from transactional activity toward stewardship of retirement systems — supporting governance, risk management, income delivery and coordination across the ecosystem. Institutions and intermediaries that help systems function better, rather than operate within silos, will increasingly define the future of retirement outcomes.